EIA: Clean Energy Grows, Climate Action Becomes More Urgent

The latest annual long-term energy outlook from the U.S. Energy Information Administration (EIA) reaffirmed that clean energy options continue to be economical and beneficial to the economy. Renewable energy resources are projected to be the second largest source of electricity by 2025. Investing in these resources will be critical to setting the nation on a path toward a clean and equitable energy economy. At the same time, the 2019 forecast warns that without significant policy action, the United States is markedly off course from realizing the clean energy outcome needed to avoid climate catastrophe by 2030 and beyond. Overall, the outlook bolsters the case that national leaders should implement policy to expand investment in clean energy and swiftly curb dangerous climate pollution.

The good news: clean energy remains cost-competitive

EIA’s outlook reaffirms that renewable energy is increasingly the economic choice to meet electricity demand, even without additional policy support.

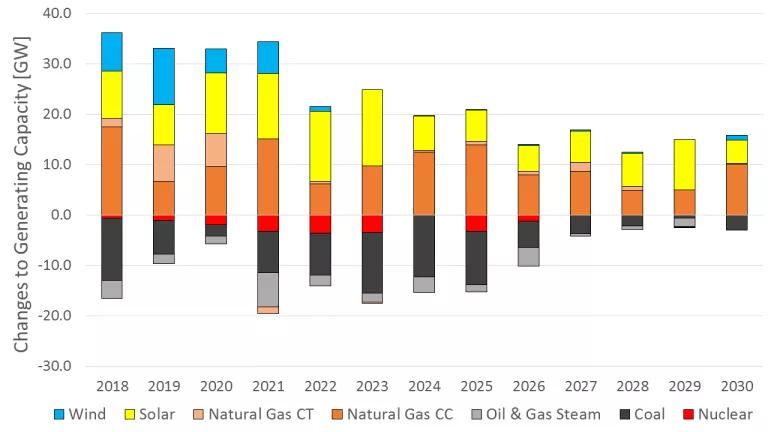

The Annual Energy Outlook (AEO) is a projection of the future with no new state or federal policies based on a conventional characterization of energy-related parameters like demand, technology costs, and fuel prices. One striking feature of this year’s outlook is that current installed solar capacity triples by 2030, as more than 100 gigawatts (GW) of new solar capacity (small- and large-scale) comes online.

Solar energy costs are rapidly declining, thanks in part to decades of innovation from the U.S. Department of Energy. We are poised to reap the rewards in the form of clean and low-cost electricity. We can even expect that clean energy growth will outpace EIA’s projections. EIA has historically underestimated clean energy development because its data inputs tend to lag the latest cost figures.

Total renewable energy output is projected to grow from 17 percent of the generation mix today to 24 percent in 2030, overtaking nuclear power in 2020 and coal power by 2025 to become the second-largest source of electricity, behind gas-fired generation.

The outlook also demonstrates that clean energy growth is coupled with economic prosperity. EIA projects that the energy intensity of the economy—the energy used per unit of economic output—declines 20 percent by 2030 as the nation’s GDP increases by 26 percent in the same timeframe. These trends extend through the entire modeled period, with energy intensity declining by 40 percent and GDP growth rising to 80 percent by 2050.

Greater investment in energy efficiency and renewable energy in the U.S. will also create millions of new jobs for people of all different skill sets and education levels. Clean energy already supports more than three million jobs across the country.

Carbon emissions declining, but more action needed

While EIA’s outlook is promising for clean energy development, the total carbon dioxide emissions trajectory is consistent with warming well above the 1.5- and 2-degree scenarios commonly associated with protecting the planet from the worst impacts of climate change. It confirms the urgency for bold and swift action to avert climate disaster.

EIA forecasts economy-wide emissions reaching 18 percent below 2005 levels in 2030. Thanks to the declining cost of clean energy technologies and new climate policies at the state and regional levels, the 2019 emissions projections for 2030 are about 11 percent lower than in EIA’s 2013, 2014, and 2015 outlooks, which projected emissions would increase through the mid-2020s.

EIA’s 2016, 2017 and 2018 outlooks showed similar emissions trajectories to the current projection, cutting emissions to between 15 and 19 percent below 2005 levels by 2030. Compared with the 2018 outlook, AEO2019 emissions are 3 percent lower in 2030, driven by renewable energy and gas generation. Yet the 2019 emissions projection for 2030 exceeds AEO2017 by 1 percent as a result of less wind deployment, significantly more gas-fired electricity, and more energy-intensive commercial buildings.

These fluctuating projections demonstrate inherent uncertainty from year to year. The differences matter because the challenge to sufficiently reduce climate-warming pollution gets more difficult as each year passes without sharply declining emissions. One recent example is the increased economy-wide emissions in 2018. The rate of emissions reductions necessary to achieve even a 2-degree warming scenario is 40 percent higher today than it was in 2013.

The Paris Accord set a target of a 26-28 percent reduction in CO2 emissions by 2025, and NRDC’s own modeling demonstrated that the U.S. must achieve a 45 percent reduction in CO2 emissions by 2030 to avert 2 degrees of warming. The more recent report from the Intergovernmental Panel on Climate Change (IPCC) showed that the world should strive to avert 1.5 degrees of warming. Measuring these goals against the AEO2019 reference case illustrates the 2030 emissions divide. Reducing emissions to within striking distance of the Paris goals by 2025 and getting on track for the emissions reductions detailed by the IPCC is only possible with ambitious but achievable policy action by all federal, regional, state, corporate and local actors.

Forecasted fossil fuel activity obstructs emissions reductions

Two primary dynamics thwart emissions reductions in the AEO 2019 trajectory. First, coal plants continue to retire up until 2025 but still represent 22 percent of the generation mix in 2030. Second, gas development booms. Gas-fired power plants, already the largest source of both capacity and generation in the country, consistently expand their share of the U.S. electricity mix through 2030.

Additionally, fossil fuel production is projected to rapidly expand. A 17 percent increase in oil and gas production in the next two years drives the United States to be a net exporter of energy by 2020 (for the first time since 1953). By 2030, production grows to 32 percent above 2018 levels, and the country is projected to export 42 percent more fossil fuels than it did last year.

A better alternative to fossil fuel production would be investing in innovative clean energy technologies like highly efficient thin-film solar panels, efficient grid-connected buildings, and energy storage to boost domestic economic productivity and energy independence. Smart policies that promote efficient consumption and technologies, like fuel economy standards for new vehicles, can eliminate energy and fuel waste from our homes and vehicles while reducing our reliance on domestic and foreign fossil fuels.

EIA’s latest forecast signals that an economy based on low-cost, clean energy is achievable, but it also highlights just how far off-track we are from securing a climate-safe future.

A safe climate and a strong economy go hand in hand. We can achieve both by investing in clean energy technologies and energy efficiency throughout the economy. This will position us closer to the NRDC long-term outlook, with the chance to cut our overall climate pollution even further to net zero. Local, state, and federal policymakers must act swiftly to expand on the clean energy progress the country is making. Succeeding in this pursuit will protect the health of children, counter the dangerous impacts of climate change, and ensure a flourishing economy.

Related Blogs

Report Recommends Improvements for State-Level Renewable Energy Siting

Southeast at a Crossroads: Bad Gas Bet or Clean Energy Boon?