Making panels where the sun shines - part 2: How India's solar manufacturing policy can more effectively support the National Solar Mission

On Friday in New Delhi, NRDC and its Indian partner CEEW (Council on Energy, Environment and Water) released our report “Laying the Foundation for a Bright Future” for the Indian audience. Attending dignitaries included Mr Tarun Kapoor, Joint Secretary of the Ministry of New and Renewable Energy (MNRE), Mr Deepak Gupta, former Secretary of MNRE, and Mr Rajinder Kumar Kaura, Secretary General of the Solar Energy Society of India. They were among more than 100 participants from across the industry including developers (e.g., Punj Lloyd), financiers (e.g., State Bank of India), and other stakeholders (e.g., Centre for Science and Environment, CRISIL). This was the New Delhi release (we released the report last week in Washington D.C. as well).

The report assesses the progress under Phase 1 of India’s National Solar Mission (NSM) through three main themes – bankability and financing of solar projects, solar manufacturing, and the enabling environment for solar in India. Let me continue from where I left off last week on Indian solar manufacturing. The first part focused on what the NSM set out to do and emerging shortcomings. This second post will delve into some of our recommendations and associated rationale for more effective policies. To start, let’s take a look at some of the key elements constituting an effective solar industry policy for India.

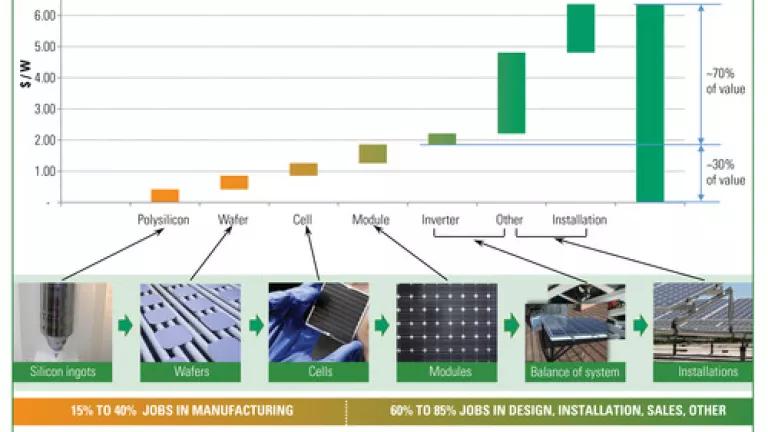

First, as outlined in the overarching goals of the Mission, the policy focus should be on areas where there is substantial value and job creation. In solar, it turns out that globally more than 50 percent of the jobs and value created is actually not in manufacturing the panels, but in areas further downstream – in inverters, balance of system, mounting, site preparation, labor, and other needs such as engineering, permitting, legal processes, financing, and distribution (see figure below). The current Domestic Content Requirement (DCR) focuses on the manufacturing of solar cells and modules, and to that extent has had limited effect in strengthening the rest of the value chain. Manufacturing is not the sole route for short-term job and value creation. Focusing sufficient and complementary efforts on the “low-hanging fruit” downstream may be more lucrative from both job and value creation perspectives in the short-term. The full benefits of manufacturing require more time to take effect.

{kind=link}

Second, an effective policy should create a level playing field, one that does not discriminate between technologies. Currently, the DCR is skewed towards silicon-based technology. Many stakeholders emphasized that the DCR was not working effectively, had led to a thin film bias, and had created considerable unused capacity at domestic silicon manufacturing factories. Therefore, a technology-neutral policy may be more judicious.

Third, an effective policy should be market enabling. At present, the DCR absolutely restricts imports of silicon-based technology and requires its manufacture in India. Some stakeholders believe that such a DCR is driving up costs by prohibiting access to cheap solar components and technology abroad. They suggested options for a less restrictive policy.

Fourth, policies need to nurture nascent industries. Currently, policies such as the customs duty structure do not incentivize solar manufacturing appropriately. India’s domestic solar manufacturing industry is not globally competitive in cost, quality or product availability. It’s a few years behind behemoth manufacturing industries in China and Taiwan, which have been considerably assisted by their respective governments. In that vein, the nascent Indian solar manufacturing industry needs comprehensive and smart government support. Indian manufacturing also needs government and private sector support in infrastructure, access to low-cost financing and raw materials.

How can these elements come together as a coherent set of policies? Our report recommends that:

- The Government of India should craft an overarching, comprehensive, and long-term policy framework that integrates policies across India and provides necessary support for the entire solar market. Such a framework should continue a nuanced focus on manufacturing, but also capitalize on the benefits available in other areas of the solar value chain such as solar services and ancillary equipment. To help with policy development, a stronger network of manufacturers able to consider emerging trade, financing and resource issues, and accordingly advise the Government, would be beneficial. Indian manufacturers are beginning to move in this direction.

- MNRE should consider tailoring the DCR to promote domestic manufacturing (tailored DCRs have had modest success in other countries). A tailored DCR could be designed to require that all PV modules be manufactured in India, uniformly enforced across all technologies.

Clearly, this would provide a level playing field. It would also facilitate a more market-based development of the manufacturing industry, because a healthy domestic module manufacturing industry at the center of the supply chain and at the divide between technology-intensive steps upstream and labor-intensive steps downstream, could catalyze further domestic development of the industry. In other words, if a domestic module manufacturing industry is established, market players can independently choose to venture into or promote downstream service-based activities, or vertically integrate into upstream manufacturing.

- As alternatives to a DCR on all modules, MNRE could consider a DCR specifying a certain percentage of solar PV components be manufactured in India (structurally similar to the DCR for solar thermal).

- Or as another alternative, a preferential tariff (higher rate per unit of electricity generated) could be provided for solar projects that utilize domestically manufactured products (as opposed to imported products). Such an approach would be less restrictive and more incentive-based, and perhaps diminish the potential for international controversy.

India has begun to unleash the huge potential of solar energy in the country by tapping into the abundant sunshine received almost year round in most regions. The Government of India (assisted by the states) has been instrumental in catalyzing the solar market’s explosive growth. Moving into Phase 2, the Indian Government, with private sector input, should develop even stronger solar industry and manufacturing policies.