Country's Largest Electricity Market Holds Power Supply Auction; Results Mixed for Clean Energy

Last Friday, PJM announced the results of its electricity power supply auction for the period June 1, 2016 to May 31, 2017. It’s a mixed bag for clean energy supporters. The good news: the results show an uptick in energy efficiency, wind and solar resources in the market, and overall lower prices for consumers. The not so good news: more coal imports from the Midwest, and somewhat less interest in “demand response” (where customers are paid to reduce their electricity demand during really hot summer days).

Background

PJM manages the flow of electricity over high-power transmission lines in 14 states in the mid-Atlantic region and parts of the Midwest. PJM also operates the largest electric power market in the world, with over 185,000 megawatts (MW) of generating capacity. In other words, PJM is BIG.

As part of its obligation to ensure that sufficient power will be available to meet future energy demand, PJM holds an annual auction for buyers and sellers of future electricity supply. The term for this supply is “capacity.” Power plants, demand response, energy efficiency and transmission lines are sources of capacity.

PJM’s auction applies to a period three years in the future, in part to give investors and developers sufficient time to develop new resources. Its auction is a little like a crystal ball into the region’s future power supply mix. Also, unlike resources in PJM’s day-ahead and real-time energy markets, capacity resources are paid to be available in the future even if their power isn’t needed to meet real-time peak demand.

By any measure PJM’s auction is big money, and annual auction revenues have ranged between $6 and $10 billion annually. To give you a sense of the dollars involved, a 500 MW power plant clearing the auction at $357/MW-day (last year’s price in Northern Ohio) would receive over $65 million in revenue for the year ($357 x 365 days x 500 MW).

There is a lot to like about PJM’s auction, although some benefits come with caveats. For example, it is a lucrative market for demand resources, but some of those resources are backed by dirty diesel generators.

This Year's Results

The clearing price was unexpectedly low in most of PJM at $59/MW-day. (In comparison, last year’s auction clearing price, for the planning period 2015-2016, was $136/MW-day in most of PJM). Prices this year were highest in New Jersey ($219/MW-day) and in some other areas. Northern Ohio, at $114/MW-day, was much lower than last year’s $357/MW-day. The auction cleared 169,160 MW of capacity, with a healthy 21% reserve margin.

PJM’s auction report is available here, and here are some more comparative stats:

Clean Energy Imacts

From our clean energy perspective, key takeaways from this year’s auction include:

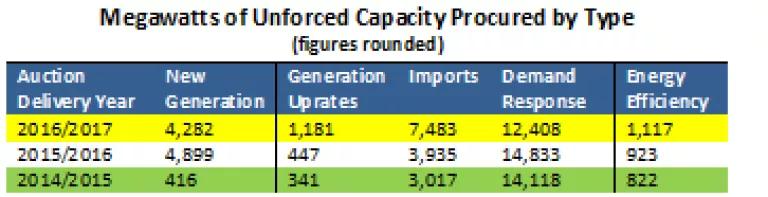

First, good news: 1,117 MW of energy efficiency resources cleared, a modest increase over last year’s 923 MW. Still, that’s only about 0.66% of PJM’s total expected peak demand of 169,000 MW.

Notably, in Northern Ohio, FirstEnergy bid far more energy efficiency resources into the auction this year than last year: nearly 200 MW versus 48 MW. We owe a shout out to our NRDC and other colleagues who earlier this year persuaded the Public Utilities Commission of Ohio to order FirstEnergy to offer more energy efficiency into the auction.

But . . . a lot of mandated and otherwise likely energy efficiency is not bidding into the auction. In Ohio alone, a recent study found that hundreds more megawatts of energy efficiency should be bid into the auction, saving consumers hundreds of millions of dollars. That means that PJM and the states need to find ways to get more energy efficiency resources into next year’s auction.

Second, also good news: the closure of up to 12,000 MW of coal power plants in PJM over the next several years will not threaten grid reliability. Lower auction prices this year, more imports and new capacity, and lower energy demand mean that coal plant owners have no basis for claiming that the EPA mercury and other standards for power plants will cause blackouts.

Third, a worrisome fact: Coal imports from the Midwest appear to be rising. Nearly 7,500 MW of imported power from neighboring regions cleared the auction, including 4,723 MW from the Midwest. Many of these power imports likely are coal power. Also, PJM may have green-lighted some plants for participation in the auction even though they don’t yet have guaranteed transmission rights into PJM. Hmmm . . . .

Fourth, mixed news: total demand resources clearing the auction declined 16% this year, from 14,833 MW to 12,408 MW. On the positive side, however, slightly more higher-value demand resource products cleared this year than in earlier years.

Fifth, more wind (871 MW) and solar (90 MW) cleared the auction this year.

The Future

Looking beyond year-to-year tweaks, we support long-term auction rule changes to expand the amount of “flexible resources” needed to complement increasing amounts of renewable energy in the grid. In other words, less need for older and dirty “baseload” power plants and more emphasis on nimbler, fast-responding gas turbines, energy storage, wind, solar, and other cleaner power.

Our colleague Mike Hogan at the Regulatory Assistance Project is a leading supporter of “flexibility” markets for electric power. His recent paper What Lies Beyond Capacity Markets is an excellent source of ideas for the next generation of electric power resource adequacy. It’s also a good reminder that PJM’s often-praised capacity market is not necessarily the best solution for the future, whether in PJM or elsewhere.

Related Blogs

Political Control of Research Funding Threatens Sound Science

We Can't Afford to Slow Down on Climate Action