Smart Energy Transition Policymaking Needs Better Mineral Demand Data

Sparse nation-level insights and inconsistent scenario designs leave U.S. policymakers ill-equipped to make responsible decisions on energy transition minerals.

Aerial (color-enhanced) view of Silver Peak Lithium Mine, Nevada

The research presented in this blog post was conducted by Swati Narasimhan, the post was written by Ms. Narasimhan in collaboration with Dr. Bustamante and Mr. Axelrod.

Understanding future mineral demand for the building blocks of the clean energy transition—including the minerals used in lithium-ion batteries, solar panels, and wind turbines—is critical in today’s policy debates. As lawmakers, regulators, and industries press for price supports and other preferential policies to back new mines, processing facilities, and recycling innovations, demand projections provide an essential data-driven foundation. However, all too often the only information before decisionmakers is too highly aggregated—such as at the global scale, or cumulative over decades—and flattens the nuanced realities about what factors drive need and how they could change in the future. National policymakers need to understand not just the reality of today’s global market for these minerals, but also how rapidly shifting conditions of technological innovation, interconnected policy commitments, and societal preferences, norms, and institutions, can shape more accurate future need assessments.

This begs the question: do today’s models of energy transition mineral demand paint a clear and useful picture of our nation’s future needs? What assumptions about the U.S.’s future are baked into these projections? And how confident can decision-makers be in projected demand figures they are presented with?

What Does the Available Science on U.S. Battery Demand Say?

To begin exploring these questions, we conducted a broad search of recent scientific studies, compiling results from numerical models of future demand for five minerals essential to lithium-ion batteries: lithium, cobalt, nickel, copper, and graphite. Most projections we found came from academic journal papers, but our search also included reports published by non-profit organizations, governments, research agencies, consultant groups, and a few private companies. We focused our search on studies scoped to the United States. Additionally, we focused on studies published in 2020 or later as representative of the most updated projections. Finally, because future demand for battery minerals will be primarily driven by the transition to electric vehicles (EVs) in the next few decades, our initial search focused on studies of demand from EV batteries as a subset of all battery or mineral demand.

What We Found: Results Vary Significantly, Depending on Future Ambition and Innovation

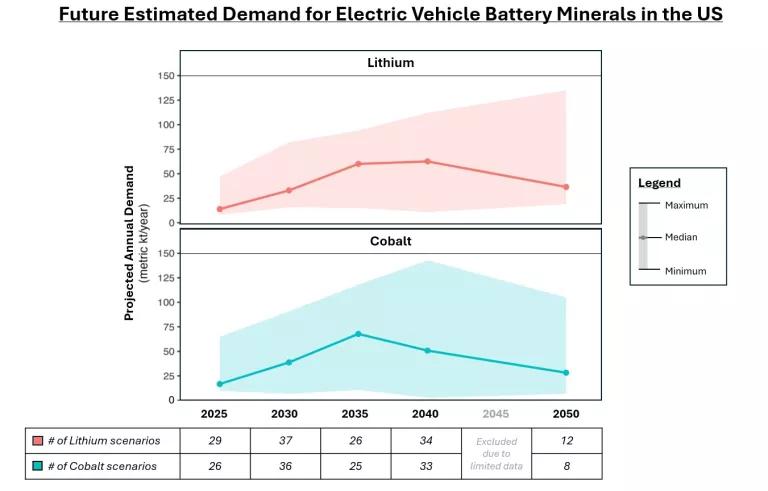

Despite the well-understood need for the five battery minerals covered by our research, we found that U.S. demand projections for several of these minerals were severely lacking. For example, despite graphite typically accounting for about 45% of the weight of lithium-ion batteries, we found only two published studies (Dunn et al. 2021 and Shafique et al. 2022) matching this scope for a combined total of four scenario projections on U.S. EV battery demand for graphite. Similarly, studies focused on nickel were surprisingly limited, with only three recent studies (Islam et al. 2021, Shafique et al. 2022, and OnLocation 2023) for a total of 13 scenario projections. Lithium and cobalt were the most widely studied. In total, we found five unique studies on lithium matching this scope (Islam et al. 2021, Dunn et al. 2021, Shafique et al. 2022, Riofrancos et al. 2023 and OnLocation 2023), reporting a total of 37 potential scenario projections for future demand over time, and four studies on cobalt (Islam et al. 2021, Dunn et al. 2021, and OnLocation 2023), for a total of 36 potential scenarios of future demand over time.

Just over half of the scenarios for both lithium and cobalt account for the effect of recycling to various degrees. At the same time, these scenarios also looked at other demand mitigating factors, such as substitution for other technology types and efficiency improvements. Looking at the aggregated EV battery mineral demand projections for the U.S., we observed significant spread between various studies’ findings. Due to their greater representation in the literature, we demonstrate that through our findings on lithium and cobalt, summarized in Figure 1.

FIGURE 1: Recent projections for future annual demand of lithium and cobalt for U.S. electric vehicle batteries exhibit significant spread. Despite matching in geographic, demand sector, and temporal scope, the modeled scenarios represent a wide variety in underlying assumptions, including corresponding U.S. climate policy scenario alignment, vehicle electrification and transportation demand, as well as technology factors, like vehicle sizes, battery operational life, mix of battery chemistries, and mineral needs per battery. Plotted results are sourced from data reported in figures and/or tables across five published studies of lithium, containing 37 different scenario projections of future mineral demand over time, and four published studies of cobalt, containing 36 different scenarios of future mineral demand over time.

Each study of demand naturally has its own underlying assumptions, limitations, and bias, so it is imperative to look at many projections together before drawing conclusions. On average, the studies we reviewed indicate that both lithium and cobalt demand are projected to grow for the U.S., at least until 2035, but not “exponentially” as is sometimes stated. In contrast, we found there were not enough numerical studies to make decisive statements about projected nickel, copper, or graphite demand for the U.S. EV sector during the time period chosen. This prevents confident, data-driven decision making about these minerals that sometimes appear on various “critical mineral” designation lists.

Without interpretation, the spread in demand projection data can create uncertainty for policy audiences. For example, there are projected scenarios where cobalt demand can remain the same or decrease beginning as soon as 2030, depending on assumptions about factors like technology deployment rates, technology mix, material use rate, and battery operational longevity. It is through the exploration of these details that decision makers can begin to make strategic and responsible decisions about energy transition mineral supply chains and mining that align with other policy goals such as minimizing environmental degradation, habitat disruption, and social harms.

Data that systematically explores the impact of technological innovations suggests that increased technology efficiency, battery chemistry changes, and recycling all can play a substantial role in changing future demand. However, strategic policy response still requires more specific and transparent data on the impacts of and opportunities for disruption by technological innovations at the national scale. Therefore, it will be essential for future studies to clearly communicate not just whether, but also to what extent, they explored demand mitigating technologies. This will prevent missing opportunities to avoid harms from excess extractive development and, if appropriate, steer policy toward other innovations to meet EV battery demand like mineral substitution and recycling.

Recommendations for Scientific Modeling Community to Increase Policy Impact

Based on the review of literature discussed above, we make the following recommendations to mineral demand modelers to increase the accessibility and impact of their research for decision-makers in government:

- Increase attention of studies focused on the U.S. EV batteries sector, especially demand projections for nickel, copper, and graphite

- Standardize terminology around model parameters and list them clearly to enable comparisons between studies (ex. underlying climate scenario; size of vehicles modeled)

- Quantify and clearly communicate model uncertainties, such as the uncertainty associated with underlying data (ex. EV vehicle demand growth; mineral requirements per battery; recycling collection rates)

- Increase attention on technological innovations like battery chemistry change and mineral recycling, and demonstrate modeled result sensitivity to these changes

Well-designed, well-defined, and up-to-date mineral demand projections are imperative for decision making across the mineral value chain to enable the clean energy transition. These scientific tools drive investment of private and public funds, future research focus, and industry strategy. To achieve the necessary “speed and scale” of the energy transition, while limiting its environmental footprint and frontline community impacts, data-driven decision making is imperative, and it begins with a more granular understanding of the many factors driving demand for these minerals.

Related Blogs

What Now for the Greenhouse Gas Reduction Fund Green Finance Programs?

EPA Announces Awards for a National Clean Energy Finance Network