Part II of this blog discusses the costs and risks of Pennsylvania's gas power build-out. The factors driving the build-out are discussed in this part.

For most of the last decade, the biggest energy story in Pennsylvania has been fracking—the use of hydraulic fracturing and horizontal drilling to extract shale gas—and the dramatic increase in gas production that fracking has driven.

The recent shift of attention to whether the Commonwealth should subsidize its nuclear plants may seem like a different narrative. But the nuclear story—which took a twist this week, with Exelon's announcement that it will proceed to close the Three Mile Island nuclear station—is very much a gas story too. It's about power plants that burn gas to make electricity, and how they've disrupted the electric generation marketplace in Pennsylvania at the expense of nuclear (as well as renewables and coal).

So Much Gas—Where to Sell It?

In 2004, when the first successful Marcellus Shale well was completed in Washington County, Pennsylvania ranked 13th in the U.S. in natural gas production. Since then, gas production has increased more than thirty-fold. Today, some 17 billion cubic feet (Bcf) of gas is extracted every day—more than in any state except Texas.

Because of fracking in Pennsylvania (and various other places), U.S. gas production rose from 52 Bcf feet per day in 2007 to 90 Bcf in 2018—a 73 percent increase. Supply quickly outstripped demand, and as a result gas prices dropped to consistently less than $4 per thousand cubic feet.

For the capital-intensive fracking industry, these low prices created a cash-flow problem that—at least so far—has been solved by the willingness of banks, private equity funds, and hedge funds to provide billions of dollars of debt and equity financing. The low interest rates that have prevailed since the Great Recession were a major driver of this willingness. But the promise of a return on all this investment depended largely on ever-increasing consumption by gas-fired power plants.

Pennsylvania has a "restructured" power sector. This means that power plants are owned not by the electric utilities (think PECO and PPL) that are regulated by the state Public Utility Commission (PUC), but by unregulated "merchant" companies that compete against each other in wholesale power markets designed by the PJM Interconnection. (PJM is the "regional transmission organization" that runs the electric grid in Pennsylvania, using markets to determine which generators sell power to utilities).

In this “competitive market” environment, companies’ decide to build new plants or retire old ones based on "price signals" from the markets. With a glut of cheap shale gas on the markets, the "price signals" from PJM said that there could be a handsome return on investment in new gas plants in Pennsylvania for three main reasons.

First, it was clear that gas could be burned to generate electricity at low cost because of the efficiency of new “combined-cycle” gas plants (i.e., more automation and fewer workers), the absence of a price on carbon pollution in Pennsylvania or PJM, and the fact that fuel costs are the biggest lifetime cost for these plants.

Second, based on the way that PJM’s markets are designed, it was apparent that the relatively low cost of operating new combined-cycle plants would translate into lower electricity prices for all generators, giving gas plants an advantage over existing plants (mostly coal and nuclear) with higher costs.

Third, PJM's markets make it easier for natural gas to make money than cleaner low-cost resources like wind, solar, and energy efficiency. Not only is there no price on carbon; PJM has designed its “capacity market” (which pays power plants to be available to produce electricity) in ways that uniquely favor gas plants. For example, PJM refuses to accept stand-alone bids for “seasonal capacity.” During the summer, this hurts both solar programs and demand response programs (the latter rely on turning down air conditioners en masse at critical times); during the winter, it hurts wind. And last year, PJM proposed changes that would push many resources subsidized by state renewable portfolio standards out of the capacity market. (Conveniently, gas generation is mostly subsidized indirectly, through tax breaks for gas production).

In the last six years, investors have put almost $13 billion into building new gas power plants in Pennsylvania. Around 9,000 megawatts (MW) of generation capacity have been brought into operation so far, including more than 5,000 MW in 2018 alone (which is more than a quarter of all new gas power brought online in the U.S. last year).

The map below, which is also available here, shows these plants, along with others that have advanced far enough in their development to seek air quality permits from the Pennsylvania Department of Environmental Protection. (You can see whether a plant has been built by clicking on the dot representing it). In all, there are more than 40 new gas power projects totaling more than 19,000 MW of capacity.

Credit: Sophia Ptacek

The Rise of Gas Generation in Pennsylvania

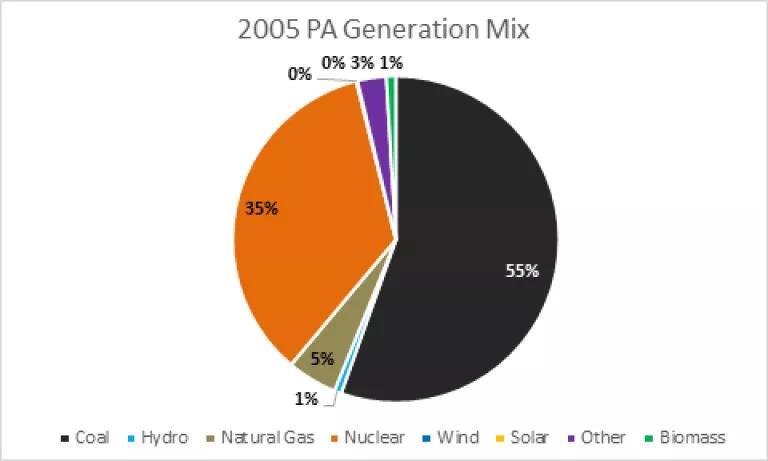

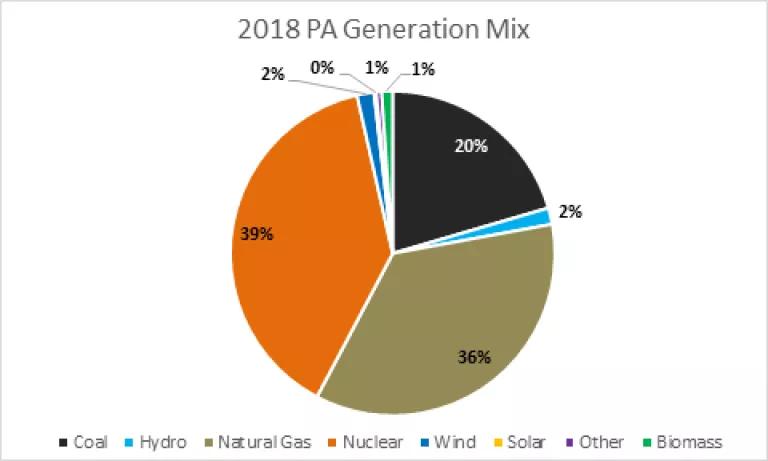

Because of this build-out, Pennsylvania is generating more and more power from gas. In 2005, gas-fired power plants produced 10.8 million megawatt-hours (MWh) of electricity in the state. By 2018, that number had risen over 600 percent, to 76.8 million MWh. So far, this increase has come at the expense of coal: between 2005 and 2018, gas-fired power rose from 5 percent to 36 percent of the state's generation mix, while coal power fell from 55 percent to 20 percent. Nuclear rose slightly, from 35 to 39 percent, and renewables (wind, solar, and hydropower) rose from less than 1 percent to around 3 percent. By contrast, the U.S. overall saw a 20-fold increase in wind and solar during the same period, from 0.4 percent to 8.1 percent.

As Part II of this blog describes, the coal-to-gas switching is cutting carbon dioxide emissions in the short term - but locking in more emissions in the long term, along with much more methane pollution.

Some preliminary modeling by NRDC projects that if Pennsylvania continues along its current energy policy path, gas generation could to rise to more than 70 percent of in-state generation by 2040, pushing offline most of what’s left of the state’s coal fleet and most of its nuclear fleet. In this case, coal would fall to just 13 percent of in-state generation by 2040 and nuclear to 11 percent (down from around 40 percent today). Renewables would remain less than 5 percent. Expected changes to PJM's capacity market would help gas even more.

When Pennsylvania restructured its power sector in 1996, the future looked like ever-increasing load growth and competition between nuclear and coal plants. No one foresaw fracking or the massive investment in gas-fired power it would drive—and there's been relatively little discussion about the climate and consumer risks of the gas build-out. Part II of this blog discusses those risks, and how Pennsylvania could chart a course toward a cleaner future. (Spoiler alert: it’s not by providing massive subsidies to nuclear plants without a "means test" to determine financial distress while doing nothing to limit carbon pollution or ramp up energy efficiency, solar, and wind).

The past and (current) future of PA's power sector. Foreground: the three smokestacks of the Hummel Power Station, a 1,124 MW gas plant built by Panda Power Funds in Snyder County, PA. Background: the four stacks of a now-shuttered 400 MW coal plant.

Mark Szybist

Related Blogs

It’s Time for PJM to Go Bold on Transmission

Governor Wolf Says Pennsylvania Will Join RGGI. Now What?