California's Landmark Solar Deployment Program - the CA Solar Initiative - has Successfully Lifted the State's Distributed Solar Industry into Orbit

The CA Solar Initiative (CSI), which got underway in 2006, is nearing its full solar deployment goal for one of its major program components approximately two years ahead of schedule. Independent analysts recently reviewed the program’s market impacts, concluding that the CSI “was the primary catalyst for change that led to the positive business environment that they [e.g. the solar industry, investors and system owners] currently enjoy.” I agree with this assessment, especially when considering the global context for which program has endured the last eight years -- global financial meltdown and resulting economic downturn, ongoing Chinese-U.S. solar trade disputes, federal-level incentives expiring, etc.

NRDC played a critical role in 2005-2006 to help create the initiative’s overall structure, goals and objectives, and made sure the policy vehicle housing all of these great ideas at the time, Senate Bill 1 (Murray), got enacted. The common understanding at the time was that solar PV was on the brink of something big - that of a global-sized, multi-billion dollar market - and the time was right for sunny California to take the next bold step to get this ever more affordable clean energy resource to the masses.

What is the CSI

The CSI is overseen by the California Public Utilities Commission (CPUC) and provides incentives for solar system installations to customers of the state’s three investor-owned utilities. The program budget is set at $2.367 billion over 10 years with a goal of reaching 1,940 MW of installed solar capacity by 2016. The CSI Program has five main components to round it out and make it more than just a solar incentive-only program. These components are:

- The General Market program, which is the main incentive program component.

- A research and development (RD&D) program, providing grants to solar technologies that can advance the overall goals of the CSI Program.

- The Single-family Solar Affordable Solar Housing (SASH) program, providing solar incentives to single family low income housing.

- The Multifamily Affordable Solar Housing (MASH) program, providing solar incentives to multifamily low income housing.

- The CSI-Thermal Program, providing incentives for solar water heating and other solar thermal technologies to residential and commercial customers

The general market program provided the lion’s share of incentives that are driving the biggest piece of the 1,940 MW goal (the general market program share is 1,750 MW to be exact). The general market program’s key innovative design feature was that of a “declining megawatt block” incentive platform – see graphic below:

![]()

This novel program structure was the result of many months of open dialogue among a wide variety of stakeholders including environmental and clean energy advocates, utilities, solar industry investors and developers, consumer advocates and perhaps most important of all, state lawmakers and regulators.

How Did the CSI Perform?

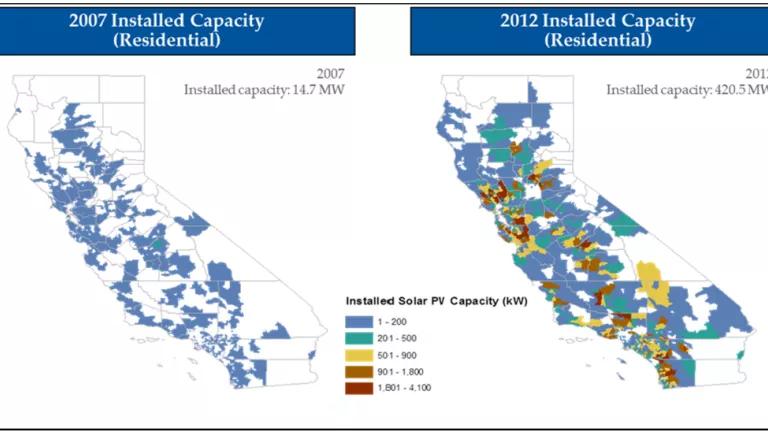

While no program structure is ever perfect, the CSI has excelled at providing three critical elements that all stakeholders agreed were most important in getting California’s distributed solar market into orbit. Those elements are: longevity, certainty and scale. The declining megawatt block structure has lowered the borrowing costs and due diligence efforts for developers, businesses and consumers to gain access to capital to purchase and build solar projects; it has helped build market confidence by educating consumers and investors on the merits of solar energy; created economies of scale in upstream supply chains and manufacturing; and made solar ever more visible with tens of thousands of new installations throughout the state.

The CSI has also led to a sustainable transformed marketplace whereby thousands of new solar installations – mostly residential – are installing solar without the need for incentives from the CSI. As much as a quarter of the market in PG&E territory and over 10% of SDG&E territory are now going up without CSI incentives.

What’s Next for the CSI

The other four components of the program continue to ensure low-income customer participation and adoption, along with scaling the market for solar thermal and applied R&D. The analysts reviewing the CSI recommend that the general market program continue to provide publicly available “market data” and other consumer-oriented information so they can make an informed decision to see what types of solar products would fit their needs and goals, and which developers and installers they can trust to do a good and honest job.

The CSI is making waves well beyond the borders of California. Earlier this year the State of New York, through its greatly expanded NY-Sun Initiative, adopted a near identical megawatt-block type program that promises to take the New York solar market into orbit just as the CSI has done for distributed solar in California. And not to be outdone, Massachusetts has now introduced legislation that also calls for a great expansion for distributed solar through a declining megawatt block program.