This is the second in a short series on the National Flood Insurance Program, some of its failings, and how it might better support preparations for our climate future. A version of this post appeared on LiveScience.com.

On July 6, 2012, President Obama signed into law the Biggert-Waters Flood Insurance Reform Act of 2012 (Biggert-Waters), putting in place long-overdue reforms. Among the most important reforms is the phase-out of certain subsidies that flood prone properties have received for decades, properties that are increasingly at risk due to rising sea levels and the increased flooding along our rivers thanks to our rapidly warming climate.

Understandably, there is pushback from some of the people who may pay more for flood insurance, which is provided and generously subsidized through the federal government’s National Flood Insurance Program (NFIP). But it’s important to understand the impact of those subsidies, the shortcomings of the NFIP in general, and why climate change makes it more important than ever to make substantial reforms.

{kind=link}

A flurry of news reports have appeared in the last several weeks in the New York Times, the Wall Street Journal, and a lot of articles in the New Orleans Times-Picayune. The stories share some common elements. They include a dramatic headline with words like “OUTRAGE” and “BACKLASH”. And the stories leave the impression that the price of federal flood insurance is going to go through the roof for all…or at least a whole heck of a lot of people…which is not quite the case.

What’s almost always overlooked is the necessity of making changes to the NFIP and the need to make even bigger changes, even faster if the NFIP is to keep up with the increased flooding challenges that climate change is bringing to our shorelines and floodplains.

Biggert-Waters: common sense reforms for a non-sensical flood insurance program

Starting this year long overdue changes are being made that will eliminate flood insurance subsidies for:

- properties that have frequently flooded and made multiple flood insurance claims;

- properties that have suffered severe flood damage or had cumulative claims that equaled or exceeded the value of the property;

- businesses; and

- second homes and non-primary residences.

Insurance premiums for these properties will rise 25% per year, but will still be receiving a subsidized rate until flood insurance premiums reflect the full cost of the risk of flooding. According to a recent analysis conducted by the researchers at the Government Accountability Office (GAO), the non-partisan and respected research arm of Congress, these changes will only affect 7.9% of all NFIP policies (437,934 out of 5,537,388 NFIP policies). Of those, only 1.2% (5,254) cover a person’s primary residence, while 98.8% of the properties slated to lose their subsidies are second homes (345,192) or business properties (87,488).

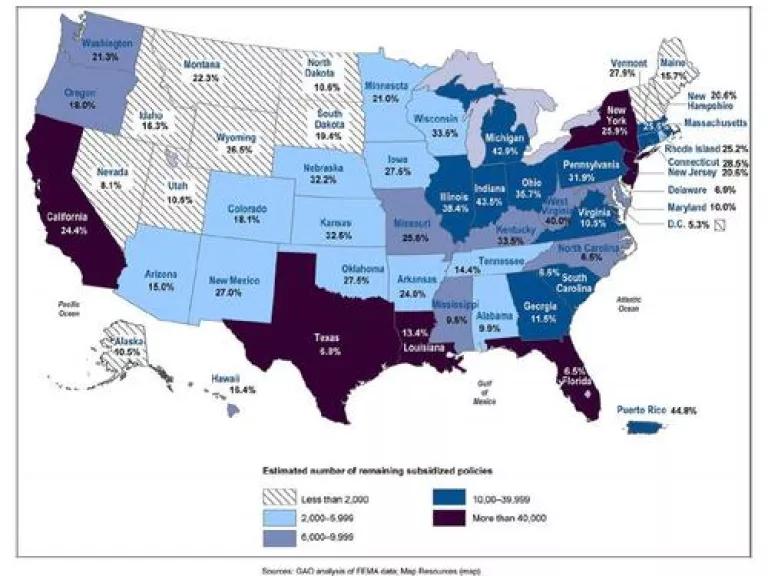

Even after these reforms go into effect, there will still be 715,259 subsidized policies issued by the NFIP, 704,230 of which are primary homes. States with the highest numbers of remaining subsidized policies are shown in the map below. As you can see, New York, New Jersey, Florida, Louisiana, Texas and California have the largest number of subsidized flood insurance policies. As a percentage of the total number of NFIP policies issued by state, Indiana, Michigan, Illinois, Ohio, Wisconsin, Nebraska, Kansas, and Pennsylvania lead the nation.

For a county by county breakdown of subsidized insurance policy holders, FEMA has created a really cool GIS map so you can see how your hometown stacks up.

More changes coming as flood maps are updated

Other subsidies will be phased out as FEMA updates its flood maps, some of which have not been revised in three or more decades. New maps have been released for all or parts of 27 states and await final approval by communities and FEMA. The new maps rely on more up-to-date hydrological data, elevation data and land use information. Not surprisingly, they show that a much larger area is at risk of flooding.

FEMA’s flood maps are so outdated they do not reflect the true flooding risks for many areas. This became quite evident in Hurricane Sandy. The areas that were actually flooded were far more extensive than FEMA’s flood maps led people to expect, as you can see in the map below. The maps undoubtedly contributed to insufficient planning and a more challenging response to flood damages that were far more extensive than what city officials and residents were prepared for.

{kind=link}

As the case of Hurricane Sandy illustrates, new flood maps will show that a lot more people are at risk of flooding. It also means a lot more people are probably going to need to buy flood insurance, since federal flood insurance is required for some properties, like those with federally backed mortgages. For the most part those properties will no longer be eligible for subsidized rates. Under Biggert-Waters, as new flood maps are approved, property owner may have to pay higher premiums or lose taxpayer subsidies when:

- a new policy is purchased;

- a property is sold;

- if they allowed their flood insurance to lapse;

- or if a property experiences severe or repeated flood-related losses.

Below is a picture that is a useful illustration of the impact of new flood maps and Biggert-Waters reforms. As maps are updated people may find that their property is below what’s known as the “base flood elevation”, which is how high FEMA expects a major flood to rise.

The top half illustrates what a policy holder would have paid for insurance prior to the passage of Biggert-Waters by Congress. The three owners of these properties would have each paid $2,235 per year for flood insurance whether the structure was 1 foot above the base flood elevation, 1 foot below the base flood elevation, or 10 feet under the base flood elevation.

Do you think those three properties are at an equal risk of flooding? Of course not. But prior to passage of Biggert-Waters, these three properties would have been treated the same, with the owner of the property at greatest risk getting a taxpayer subsidized incentive to live in a risky, flood prone area.

{kind=link}

The bottom half of the picture illustrates how things will work in the future, as new flood maps are approved and as actuarial rates are assessed. The person who has property 1 foot above the water when it floods will see a savings of $1,506. And the property that is ten feet underwater when it floods? They’ll pay more….alot more.

But these higher actuarial, or risk-based, insurance rates will only happen once flood maps are updated and if the property owner sells the property, allows their existing policy to lapse, or suffers severe or repetitive flood damage. And the increase will be phased in over a 5-year period.

Should someone who’s property may be ten feet underwater during a major flood (and probably under water more frequently, even during minor floods) pay more for flood insurance? The answer is yes, according to the actuaries and risk-analysts whose decisions are based on what the facts and numbers say. If you are more likely to flood, it’s fair that you pay a higher price, because you’ll probably be filing more claims and receiving more insurance payments. That’s how risk-based pricing and actuarial rates work.

And the numbers show why. According to data compiled by the Federation of American Scientists, properties that have been flooded multiple times made up 3% of NFIP policies but accounted for 35.0% of the claims and 29.8% of the damages paid out between 1972 and 2011. Until Biggert Waters was passed, those property owners received a subsidy for living in such a risky location. Now, the small number of properties that are most at risk and have been the biggest financial drain will be required to pay a fairer share.

Dirty Little Secret…the new maps don’t believe in climate change!

Even as FEMA updates its flood maps with the latest and greatest hydrologic, elevation and land-use data, they neglected to factor in the little problem of climate change. The new and improved coastal flood maps don’t contemplate the anticipated rise in sea levels. And updated flood maps along rivers and streams do not factor in the predicted increase in storm intensity and related flooding.

Oops.

That means the maps FEMA has generated to date in 27 states are, at best, still wrong and still under-predicting the true extent of future flooding.

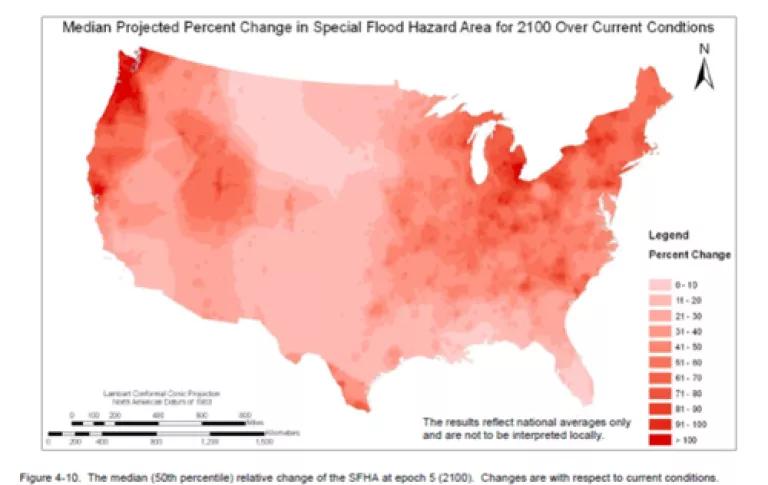

In June a FEMA analysis was released that estimated just how much more of the country will be at risk of flooding because of climate driven sea-level rise and extreme weather, as the map below shows.

On average coastal areas are expected to see a 55% increase in size of areas prone to flooding, mostly along the Eastern seaboard, the Pacific Northwest, and the Great Lakes. Increased flooding is projected even in areas that are expected to be more arid and dry, due to the intense and flashy nature of future storms as the climate warms.

The number of NFIP policy holders along rivers will likely increase by 80% by the year 2100 and the number of coastal policies may increase by 60% to 130%, depending on whether we begin to move population away from the coast or we try to keep our population in place – and in harm’s way.

As a requirement of Biggert-Waters FEMA is convening a Technical Mapping Advisory Council to recommend how best to incorporate climate impacts into future flood maps. That Council’s recommendations should be released soon and it would be a shock if FEMA is not told that climate change impacts have to be factored into any new maps.

What Next?

Biggert-Waters has gotten the latest debate going about the wisdom of subsidized flood insurance. It’s also hinted at just how much is at risk due to climate change. The move to risk-based pricing of federally backed flood insurance and the elimination of some of the most problematic subsidies has exposed how big of a problem we’ve made for ourselves. And that includes a $20 billion debt owed by NFIP as of November 2012, which will likely climb to about $30 billion once all claims from Hurricane Sandy are paid out.

We still need to find a way to help people that may be put in economic distress by increased flood insurance costs. Those people should not be left without a safety net, nor should they be left in place to be flooded again (and again, and again). We know they need help and we know the risk of flooding is on the rise.

The fact is that subsidized insurance and out of date maps led to millions of people moving into flood prone areas. The National Flood Insurance Program should have helped manage our nation’s risks from flooding. If it had been properly designed and implemented, it probably would have helped avoid billions of dollars in past damages, and perhaps been a very useful tool for managing climate risk as well.

Instead it evolved to become a liability. But now, the United States is starting to wake up to the problems and Biggert-Waters has started a conversation about how we fix them. Hopefully we can fix the problems faster than climate change exposes them.

On August 2nd I posted about some historical failings of the National Flood Insurance Program that have led to it being a financial drain on the nation as well and its failure as a program to manage the nation’s flooding risks.