Principles for Harmonizing State Policies with Markets

The Federal Energy Regulatory Commission’s conference on how state policies (such as renewable energy procurement targets) interact with regional electricity markets highlighted a variety of problems that decision-makers and stakeholders will have to prioritize and clearly formulate in order to helpfully resolve tensions. I testified at the conference, and here is what I recommended in order to (1) harmonize state policies with the markets, (2) ensure the markets do not discriminate against clean energy, and (3) enable electricity customers to cost-effectively obtain what they want from the market.

My testimony focused on PJM, which operates the electric grid for 61 million customers in DC and thirteen Mid-Atlantic and Midwestern states. PJM runs the largest “capacity market” in the world, where natural gas, coal, nuclear, and a small amount of clean energy resources compete for commitments to deliver electricity in the future. (This commitment is the “capacity” and resources are separately paid for actually delivering the electricity through the energy market.) The lowest bidders in annual auctions win the ability to provide capacity and get paid for that commitment. The market thus signals cost-effective resources to enter or stay in the system and inefficient, expensive resources to retire.

Following the fracking boom, a glut of natural gas supply has driven down capacity market prices, pushing out the least efficient nuclear and coal plants. (A recent report found that cheap natural gas contributed ten times more than environmental regulations to the decline of coal in the past decade.) This has led states with coal and nuclear plants that didn’t receive capacity commitments to push for legislation to subsidize their plants, which would then be able to offer into the markets at lower prices. From certain generators’ and PJM’s perspective, enabling resources that receive subsidies to bid in below their real costs “suppresses” the market prices, and they’re seeking to remove these resources or subsidies from the market to bump up their revenues. The scope of this subsidy hunt has grown to include (and sometimes focus on) renewable energy procurement targets and incentives, like state renewable portfolio standards.

How the problem is formulated will affect whether the solution helps or frustrates state policies.

The first problem with focusing on what to do with subsidies in the capacity market misses the real problem—these state measures exist because states cannot directly select the attributes or types of resources they want from the “market.” Unlike a traditional market where customers can voluntarily buy what they want in quantities they desire, PJM’s capacity market only offers one kind of product (and PJM determines how much consumers in the market must buy). Namely, customers must buy the cheapest capacity with winning bids in the market regardless of their preferences for emissions-free or local energy resources. It’s like limiting customers to buying the cheapest food at the supermarket regardless of their preferences for organic or food from nearby farms.

To make matters worse, seasonal produce is largely unavailable in this market. Certain capacity resources, like wind and solar, are largely excluded from the capacity market because there is an arbitrary requirement that capacity can only be transacted in year-long increments. A summer and winter capacity period of six months each would cover a full year just as well, and would better enable resources that are stronger in the summer (solar) or winter (wind) but are not uniform throughout the year to provide capacity. So, in PJM’s market, we’re stuck buying things that can sit on the shelves all year.

Indeed, there is a gross mismatch between what PJM’s customers and states want and what its market sells. PJM’s mix of capacity resources is about 1 percent wind and solar, but PJM states support much greater amounts of clean energy on the grid as demonstrated by their renewable portfolio standards (ten states in PJM and DC have them) and participation in the Regional Greenhouse Gas Initiative. Also, polls have shown strong bipartisan support to accelerate clean energy adoption and the vast majority of people in all thirteen PJM states and DC support requiring their utilities to produce at least 20 percent of electricity from renewables.

Essentially all resources receive some form of incentive or preferential treatment; focusing on the most visible would discriminate against and undermine the programs with the most public support while leaving intact policies that have not been vetted by the public.

The second major problem with trying to extricate state policies from the market is that virtually all resources receive some form of incentive or preferential treatment. To identify and disentangle the effects of all government interventions in a principled and non-discriminatory manner would be at best administratively burdensome and most likely near impossible to do.

It would be discriminatory and result in adverse policy outcomes to focus on the most visible state policies, such as renewable energy programs that that enjoy a great deal of public support, while ignoring the wide swath of fossil subsidies, which tend to be embedded in more obscure tax provisions, government funding appropriations, and preferential zoning and setback rules that favor fossil development over renewables. Fossil fuels also benefit from taxpayer-funded site clean-ups and road repair from damage incurred in transporting fuel.

Further, only now beginning to focus on current state policies disparately targets newer resources and technologies, while ignoring the subsidies incumbent generators have enjoyed for decades, which have enabled them to scale up and build out infrastructure. For example, the natural gas industry has been receiving tax breaks since 1913, and the coal industry since 1932.

Capacity oversupply is likely the biggest factor driving down prices, which are signaling excess capacity to retire.

The third problem with targeting subsidies to address “low” prices is that it misses potentially larger drivers of the same effect—falling electricity demand and a flood of new gas supply are driving down the price per unit of capacity (measured in megawatts). Around 5,500 megawatts of new gas entered the market despite record-high supply and at prices much lower than what analysts thought new generators would need. Analysis shows that the new gas brought prices down by 12 to 25 percent in PJM. And more gas is projected to come online—another 20,000 megawatts by 2019—which will exacerbate the problem.

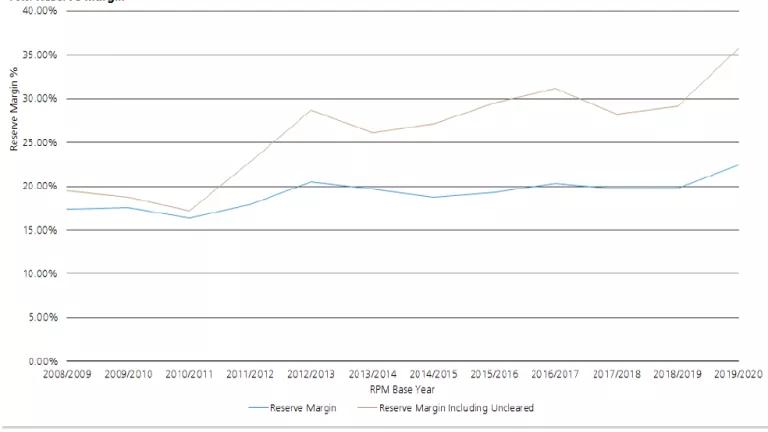

PJM normally procures a little extra capacity, around 16 percent just to be safe, but PJM obtained a record-high excess of 22.4 percent in its latest main auction and that excess increases to over 35 percent if we include capacity on the system that did not receive payment. (A recent assessment bumps the excess committed capacity up to 29 percent for this summer.)

According to basic economics, a low price in an oversupplied market is a signal to retire excess capacity—it’s not an indicator that generators are not paid enough.

Regulators should be concerned about capacity oversupply, especially when customers are paying for too much of it, as they are here.

Some principles for formulating a Federal Power Act compliant solution that respects state policies.

The Federal Power Act requires that FERC ensure the rules it approves to be "just and reasonable" and not unduly discriminatory. There are a few solutions regulators could adopt, but any principled solution should:

- Not discriminate between resources by focusing on certain “subsidized” resources because essentially all resources receive incentives or preferential treatment;

- Avoid overcharging customers by reducing excess supply;

- Respect state authority—market rules should not undo state policy choices;

- Enable state-policy supported resources to displace other generation and prevent inefficient entry of new conventional resources to avoid over-procurement (which follows from the previous two points); and

- Provide flexibility for customers to buy what they want from the market or opt-out to obtain capacity outside of PJM’s market.

Related Blogs

U.S. 2035 Climate Target Is Ambitious, Achievable & a Call to Action

COP29: Key Outcomes Signal Need to Deliver Greater Climate Action