National elections are underway and dominating headlines and conversations across India. In parallel, the timely release of the second new consensus report from the U.N.’s Intergovernmental Panel on Climate Change (IPCC) documenting the impacts of climate change, has confirmed again the current and growing risks to the economy, human health and food supply of India’s communities. This latest warning of the growing impacts of climate-fueled disasters should refocus attention on the country’s efforts to mitigate and adapt to climate change.

After a bumpy year, India’s renewable energy efforts are offering tentative but promising signs that clean energy is ready for resurgence. But it remains to be seen whether the solar and wind energy industries will work together to learn from each others’ experiences and grow the whole clean energy market. And whether much-needed support for the renewable energy market will increase to enable clean energy to emerge a winner in India.

The recent slowdown of India’s renewable energy industry is well-documented, but with the current peak energy deficit hovering around 9%, it is clear that the status quo dependence solely on fossil fuel is neither sufficient nor sustainable. Renewable energy sources can power India's future, offering the country a cleaner, more sustainable way to supply its communities' growing energy needs. In addition to policies that prioritize energy efficiency in the country’s buildings and appliances, clean energy—particularly solar and wind energy—is key to reducing the strain on infrastructure and increasing energy security.

Despite unclear market signals and a dip in India’s investments in renewable energy last year, it appears both the domestic solar and wind markets could be headed toward a more positive 2014 based on recent developments:

India’s Solar Market Offers Promising Signs of Improvement

The solar market is recovering from a rough year of setbacks, including an international trade dispute, reduced investments, slumping solar sales, and delays in both the Mission’s Phase 2 and state solar auction allocations. Despite this, the Ministry of New and Renewable Energy (MNRE) reported that India added more than 1 gigawatt (GW) of solar energy to its grid last year, nearly doubling the country's cumulative solar capacity. With many grid-connected solar projects commissioned by state solar projects coming online in early 2014, the country now has more than 2.6 GW of installed capacity as of the end of March.

Another good sign for solar energy was highlighted by National Solar Mission's successful bidding process for its first batch of Phase 2 projects in Q1 2014. Bids for these National Solar Mission-sponsored solar projects were more than three times oversubscribed by solar developers for the 750 MW of available photovoltaic capacity. MNRE also announced plans to auction an additional 250 MW worth of solar photovoltaic power in 2014. Many of these projects are expected to come online in 2015, meaning the country could see another jump in its solar power capacity next year.

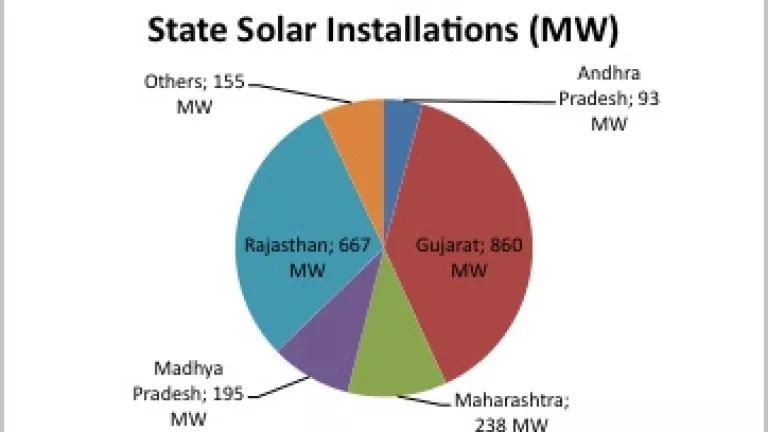

Gujarat, the current state leader for installed solar, is increasingly having to share its title with emerging state powerhouses Rajasthan and Madhya Pradesh, who are receiving strong interest from solar investors. Newer rooftop solar energy programs, like Tamil Nadu’s scheme that is under 6 months old, have received promising responses from developers too.

State Solar Installations in India as of January 31, 2014:

{kind=link}

© CEEW, NRDC based on data from MNRE’s “State wise Installed Capacity of Solar PV Projects under Various Scheme as on 31.01.2014,” available here.

Government policies can support this process, especially as the prices of solar energy products continue to decline. The government can work with banks to overcome the persistent perception of risk and unfamiliarity associated with solar financing. Innovative financing and incentives to invest in solar technologies can harness the high level of interest in solar energy present in India and act as the bridges that bring solar investors and consumers together. On this front, our NRDC team and our partner, the Council on Energy, Environment and Water (CEEW), are working with government agencies, developers and financiers to support the growing solar market both on the economic policy front and in overcoming financing barriers.

Stay tuned for our team’s release of a forthcoming series of publications that offer specific findings and recommendations to ease financing for grid-connected and decentralized solar projects in India and bolster local job production.

Signs of India’s Wind Market Reenergizing

Wind power in India has an estimated total potential of more than 100 GW in India, which was slightly less than half of India’s total electricity generation capacity in 2013. Although India already has the fifth largest wind generation capacity in the world at 20,000 MW, recent policy shifts have temporarily slowed wind energy’s momentum.

To reverse this trend, MNRE recently announced plans to launch a National Wind Energy Mission (NWEM). The NWEM will operate differently than the National Solar Mission. Rather than inviting bidding for projects, MNRE will play the role of a "facilitator" to strengthen grid infrastructure for wind power, identify high wind power potential zones, clear hurdles for land issues, and regulate wind power tariffs. Measures such as accelerated depreciation (a valuable tax benefit that reduces current taxable income) and a generation based incentive (which provides an additional tariff to developers for wind electricity fed into the grid), which were curtailed in 2012, are expected to be reintroduced under the NWEM.

As with solar energy, there are many potential avenues to scale wind energy beyond the NWEM. States with large wind potentials – including Gujarat, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan, and Tamil Nadu – can introduce their own schemes to promote wind energy. State and central government policies can be implemented right from the start of the NWEM to ensure sufficient financing wind projects and avoid repeating the hurdles the National Solar Mission launch faced.

Increasing Indian financial institutions’ comfort levels and ability to affordably fund clean energy are key to increasing renewable energy investments. Ensuring that the wind and solar industries are learning from each others’ experiences can also help both markets grow and succeed. By working with financial institutions to establish effective financing policies, instruments and mechanisms, India can support and enable a needed resurgence in the diverse renewable energy projects and products that can sustainably power its future and help mitigate climate change’s worst impacts.

Co-authored by Gaurav Bansal and Meredith Connolly