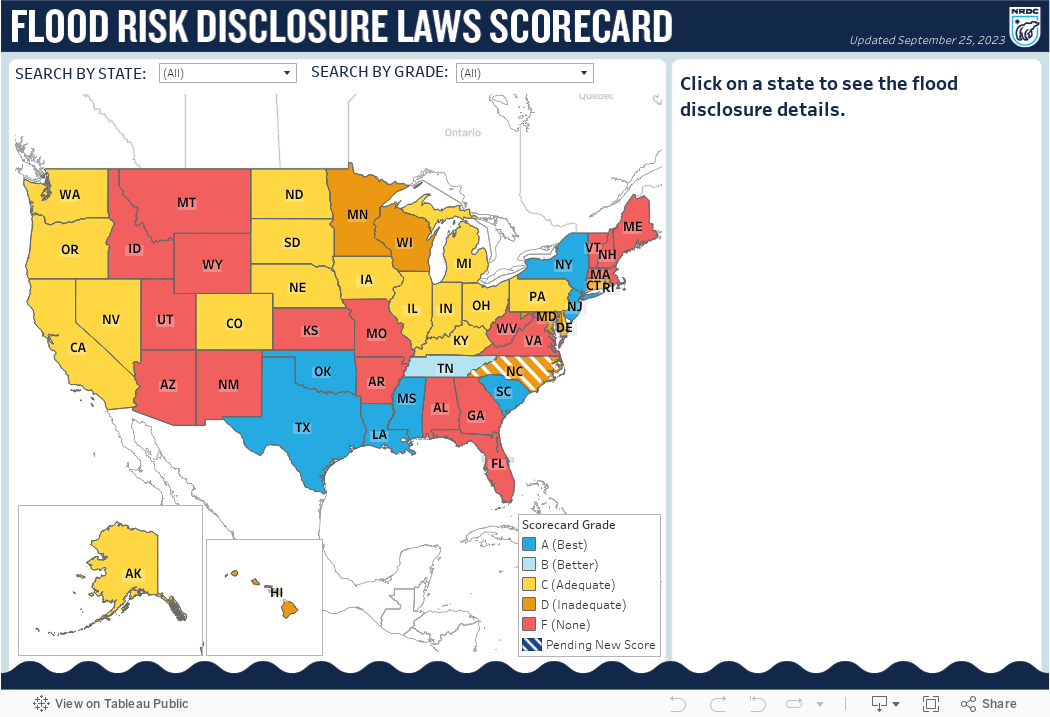

How States Stack Up on Flood Disclosure

Millions of Americans live in homes at risk of flooding, and a home that has flooded once is likely to get hit again.

Steve Bohnstedt/Quincy Herald Whig via AP

Millions of people live in homes that are at risk of flooding, and a home that has flooded once is likely to get hit again. Unfortunately, it’s extremely difficult for a home buyer to learn of a property’s flood history. That’s because many states do not require home sellers to disclose past damages to potential buyers.

An NRDC-commissioned report found that home buyers who unwittingly purchase a flood-prone home are likely to incur tens of thousands of dollars in flood-related damages. By denying home buyers information about past flooding, people cannot make informed decisions about one of their biggest financial investments—their home.

Explore the map to see if your state’s real estate disclosure laws leave you in the dark when it comes to flooding:

Many home buyers are completely unaware of whether their supposed dream home has flooded before. Too many homeowners learn of their property’s propensity to flood only after suffering through multiple disasters. You may think you’ll be told if the home you’re buying has been underwater before, but that is not guaranteed.

Learn More: Flooding & Financial Risk

More than one-third of states have no statutory or regulatory requirement that a seller must disclose a property’s flood risks or past flood damages to a potential buyer. The other states have varying degrees of disclosure requirements. This hodgepodge of state and local policies hinders buyers from making fully informed decisions.

In fact, many Americans who are about to make one of the biggest financial investments of their lives have zero knowledge of whether a house has flooded and is likely to flood again. This problem could be solved simply by having access to information—information that the seller of the home may have. And if the previous owners had flood insurance through the National Flood Insurance Program (NFIP), the country’s program to provide low-cost insurance to people whose homes are susceptible to flooding, then the Federal Emergency Management Agency (FEMA) would have a record of past flooding it could share too.

The NFIP must do more than just help homeowners quickly rebuild after a flood—the program must also ensure that all homeowners and home buyers have a right to know a property’s history of flooding and risk of repeat flooding. Congress must reform the NFIP to make it easier for people to access flood hazard information. The more information current or prospective homeowners have, the better equipped they are to avoid purchasing a flood-prone home or to take measures to reduce the risk of damage. This information would not only benefit homeowners, but also taxpayers’ pocketbooks. Floods create a heavy burden for the country’s disaster response budget and the financial stability of the NFIP. As climate change fuels sea level rise and more extreme weather, the need for greater transparency of flood risks will become only more imperative.

All prospective homeowners should have access to information about past flood damages and flood risks so they can protect themselves and their property. The consequences of not having this information can be financially ruinous.

Homebuyers can unknowingly purchase a previously flooded home and incur tens of thousands of dollars in unanticipated damages as a result. NRDC commissioned a report by the actuary firm Milliman, which examined 25 states with inadequate disclosure requirements. That report found that thousands of people likely bought a previously flooded home without ever being told that information. On average, those unsuspecting homebuyers could incur tens of thousands of dollars in unexpected damage.

NRDC’s 2022 report by Milliman, which examined how the lack of disclosure negatively impacted homebuyers in New Jersey, New York, and North Carolina, was instrumental in convincing those states to make major updates in their disclosure policies. New York and New Jersey passed legislation that moved them from failing grades on NRDC's disclosure scorecard to an A. In North Carolina, the state's Real Estate Commission amended its mandatory disclosure form to go from a D to an A.

To close the current information gap, NRDC will continue pushing for reforms by states. We are also pushing FEMA to put in place a nationwide flood disclosure requirement, through the NFIP. NRDC recommends the following actions:

- States need to update their inadequate disclosure laws to provide home buyers with the right to know whether a home has ever flooded, how often, what it costs to make repairs, if the home is located within a designated floodplain, and if flood insurance is required on the property.

- As a condition of NFIP participation, FEMA must require states to adopt comprehensive flood hazard disclosure requirements for real estate transactions. FEMA is now considering implementing this through either regulation or changes in statutes.

- Upon request, FEMA should provide homeowners with information about their property’s history of flood insurance coverage, damage claims paid, and previous owners’ receipt of federal disaster aid, which would require the purchase of flood insurance or risk being ineligible for federal disaster aid.

- FEMA should create a public, open-data system with information related to flood-damage claims, repeatedly flooded properties, and communities that are properly enforcing local building and zoning codes required under the NFIP.

Disclosure Grade

States are graded on a scale of A to F corresponding to the quality of the state’s flood hazard disclosure law (i.e., the level of flood hazard information required to be disclosed). States with a grade of F have no statutory or regulatory requirements for a seller to disclose a property’s flood risks or past flood damages to a potential buyer. However, many of these states have private Realtor associations that provide voluntary disclosure forms referencing potential flood hazards. States with grades of A to D have statutory or regulatory real estate disclosure provisions that mandate a seller to disclose to a potential buyer flood hazard information associated with the property.

Grade A (Best)

Requires disclosure of whether the property is in a designated floodplain, whether there have been any flood damages to structures on the property, and whether there is any requirement to carry flood insurance. Also requires additional disclosures, such as the cost of flood insurance or an elevation certificate.

Grade B (Better)

Requires disclosure of whether the property is in a designated floodplain, whether there have been any flood damages to structures on the property, and whether there is any requirement to carry flood insurance.

Grade C (Adequate)

Requires only the disclosure of whether the property is in a designated floodplain and whether there have been any flood damages to structures on the property. Fails to require disclosure of whether flood insurance is mandatory. While some states require disclosure of whether flood insurance is maintained on a property, this provision fails to address a situation in which the current owner does not carry flood insurance even though such insurance is required, for instance, due to receipt of federal disaster aid.

Grade D (Inadequate)

Requires only the disclosure of whether the property is—before point of sale—in a designated floodplain. Fails to require disclosure of any flood damages to structures on the property or disclosure of any requirement to carry flood insurance.

Grade F (None)

No statutory or regulatory requirements for a seller to disclose a property’s flood risks or past flood damages to a potential buyer.

This page was originally published on August 19, 2024, and has been updated with new information and links.

This information is provided for general informational purposes only, and may not reflect the current law in your jurisdiction. This information does not provide legal advice and does not create an attorney-client relationship. If you need legal advice, please contact a licensed attorney in your state or other appropriate licensing jurisdiction.

Related Resources

Occupational Heat Safety Standards in the United States

1.5 Degrees of Global Warming—Are We There Yet?