Southeast at a Crossroads: Bad Gas Bet or Clean Energy Boon?

The Southeast is facing a spike in electric load growth projections. Utilities are proposing a massive gas buildout to meet it—we can do better.

The city of Atlanta, Georgia

Cameron Venti

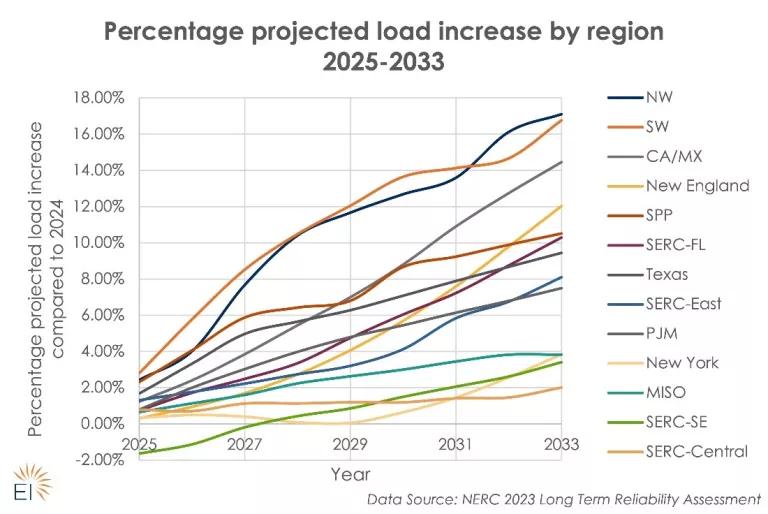

It's hard to open your inbox or a newspaper these days without running into some coverage or reports about the dramatic recent increase in electric demand in many parts of the nation. This follows decades of nearly flat demand—an era that now “appears to be over.” However, at times like these, it’s also important to take a deep breath and dig in to the precise profile of that new demand in order to craft smart solutions to meet it, as our colleague Tyler Norris recently pointed out. That said, the figure below illustrates the very real trend emerging across the country.

Meeting Growing Electricity Demand Without Gas, Energy Innovation

But that trend is not monolithic across all regions: Ground zero is the Southeast. The good news? Some of this increasing demand is—in cases such as clean tech manufacturing—directly related to increases in economic development and jobs. With the tailwinds generated by the Inflation Reduction Act, Bipartisan Infrastructure Law, and CHIPS Act at the federal level, we’re seeing an unprecedented onshoring and reshoring of clean tech manufacturing such as electric vehicle (EV) battery factories and other industrial development, as well as anticipated increases in EV adoption and building electrification driven by those federal policies along with state and local efforts.

At the same time, data centers (and more speculative cryptocurrency mining operations) are proliferating in some parts of the country. The challenge? This trend also means that regional utilities—and the state commissions that regulate them—are scrambling to craft plans to meet that new load. (Our friends at Energy Innovation recently published a great primer on these issues; the figure above is pulled from that report.)

This demand surge puts the energy transition under the spotlight. Grid planners and stakeholders can respond to this challenge by accelerating the adoption of clean resources and stabilizing the grid with abundant affordable and reliable resources already waiting to get online. Or they can panic and squander this opportunity by doubling down on what in many cases are far-costlier fossil fuel investments.

The consumer and emissions stakes are massive

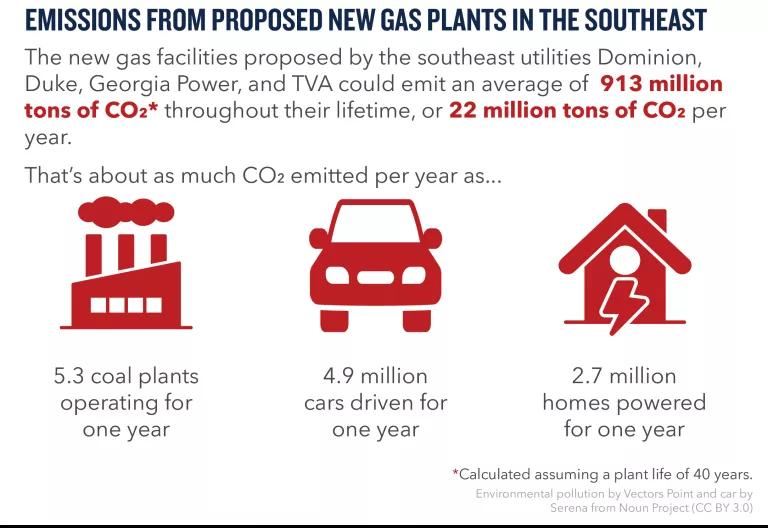

Collectively, it is estimated that the new gas plants being proposed by Dominion in Virginia, Duke, Georgia Power (a Southern Co. affiliate), and TVA alone—if built—would amount to more than 14 GW of new gas in the next few years (this GW number would be even higher if you include the gas plants proposed by all the utilities in the region). This at precisely the same time when the U.S. Environmental Protection Agency (EPA) is poised to release carbon standards limiting emissions from fossil-fueled power plants. As a result, this potential massive gas buildout in the near-term jeopardizes meeting emissions reductions targets, 2030 targets for utilities and corporate entities, and threatens affordability, with customers on the hook for potentially expensive, dirty, and ultimately stranded assets that may or not be usable for their typical, carbon-intensive lifespans.

To be clear, in some instances there may very well be a justified need to build some very limited, narrowly tailored peaking combustion turbine (CT) gas capacity that will run for only a limited number of hours across a given year, at times of peak demand in winter or summer depending on the locale. But it is an open and fair question as to whether the scale of proposed capacity across the Southeast is in fact the right path forward—and one worth shining a brighter light on to get it right.

The graphic below shows the magnitude of the emissions these new facilities could drive over the next 40 years, accounting for typical capacity factors from CTs and combined cycle plants as proposed.

Maeve Sneddon/NRDC

How does the Southeast compare with the rest of the nation?

Grids across the country are forecasting significant load growth but are—for now—managing it without the reflexive rush to gas that we’re seeing in the Southeast. Case in point: The nation’s largest regional transmission organization (RTO) consisting of 13 states, PJM, has a queue of proposed projects that is made up of 94 percent renewables. Admittedly, its interconnection process is far from perfect, resulting in a significant backlog of getting projects online, but the prevalence of clean energy being proposed and financed there is in stark contrast to what we’re seeing play out in the Southeast. And this recent LBNL report has a great national summary of a huge number of clean energy projects stuck in the queue backlog across the country.

It is also essential to provide customers more tools to keep costs down. If data center operators can shift their tasks around the country when the grid is stressed in one region, it can drive significant savings for all customers by avoiding the need for new power plants. Markets that let them earn these savings have allowed this to happen. Demand response, energy efficiency, and distributed energy resource programs let customers see the value of controlling their energy usage. While southeastern utilities have some of those programs in their portfolios at varying degrees of effectiveness, much more can be done to squeeze every drop out of those vital demand-side solutions—not only at the commercial level to mitigate new spikes from data centers but also through aggressively ramped up baseline energy efficiency/weatherization programs in the residential sector (especially for low-income customers who need those savings the most).

The Southeast isn’t alone in its growing power demand, but the makeup of its power sector presents a somewhat unique opportunity for fossil fuel interests to get in while the getting is still good and turn a digital and industrial boom into yet another gas boom. Gas is a riskier investment than renewables and storage, which is why, for the most part, only utilities with a guaranteed rate of return are willing to make this bet. But gas prices are extremely volatile and subject to significant price shocks since there are supply constraints and increasing exports. In North Carolina specifically, Duke Energy customers have suffered huge bill increases from those higher, volatile natural gas prices, which is another reason why overreliance on this fuel is terrible idea.

But it doesn’t have to play out this way. It is entirely possible for utility commissions in a vertically integrated state to steer their utilities in a cleaner, less risky direction for their customers. More on what that better approach looks like below, but we’ve seen as much in some other regions, such as Tri-State's recently approved resource plan in Colorado.

Those good outcomes won’t happen without a change. The status quo regulatory environment in the Southeast makes fossil fuel projects appear “easy” to build, while presenting unnecessary barriers to building out the clean, flexible, less risky solutions that will benefit ratepayers and reliability in the long-term. We’re hopeful that commissions and the utilities they regulate do right by their public and correct course.

Latest developments in Georgia

The most recent related outcome involves the Georgia Public Service Commission’s (PSC) pending approval of Georgia Power’s proposal to build out multiple new gas turbines to meet projected load growth in the state.

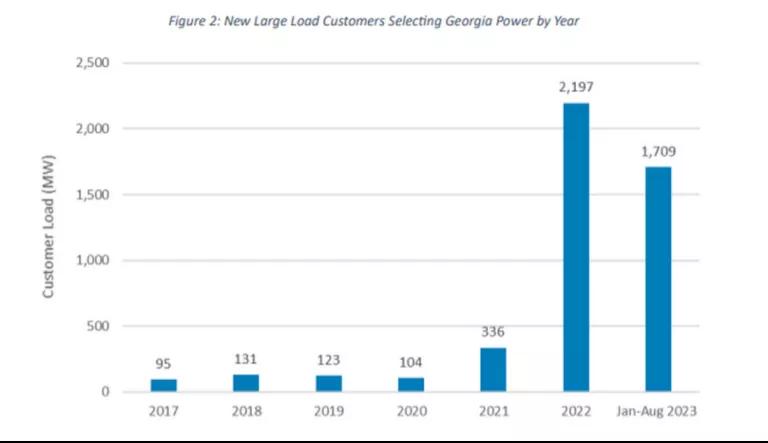

Last year, Georgia Power filed an unanticipated update that was outside of typical procedural timelines—which the company pursued due to a marked surge in load growth, primarily from new and expanded data centers (for context, these facilities need power 80 to 90 percent of the time across a year and can constitute the equivalent electric demand of 10 Super Wal-Marts). This growth, nearly 22 times the historical average, prompted the utility to request a number of measures to accommodate it, including a purchase power agreement with Mississippi Power and extending the life of some fossil generation facilities.

Georgia Power 2023 Integrated Resource Plan Update, October 2023

As a result, Georgia’s PSC staff struck a stipulation deal with the utility just minutes before a late March rebuttal hearing, granting most of the utility's requests. The stipulation includes approval for three new gas combustion turbines with a 46-year lifespan; broad discretion for transmission projects; a lower commitment to renewables than was on the table in that docket; and an expedited RFP process, potentially at a greater cost to ratepayers relative to alternative approaches. (This at precisely the same time recent reporting found that Atlanta residents are facing the fourth-highest energy burdens of any city in the nation.) And of particular note, the U.S. Department of Defense (DOD) has come out in strong opposition to the stipulation due to its heavy reliance on gas and limited clean energy solutions, which makes it harder for the DOD to meet its mandate to decarbonize at its Georgia facilities.

Meanwhile, right next door, Duke Energy is currently proposing an even more alarming number of gas plants, despite the fact that North Carolina has a law on the books calling for a 70 percent reduction in electricity sector carbon emissions from 2005 levels by 2030. (Despite rumblings, we remain hopeful that Duke doesn’t attempt to undermine that existing law in the coming months.) A future post may dig into the details of that ongoing proceeding and the broader power sector issues facing the Carolinas.

Reliability is paramount—but there are better ways to get there

NRDC has always recognized the importance of maintaining the reliability of the grid even as we aggressively work to decarbonize it. Does this uptick in electricity demand seem “real”? Certainly. (Although we’ll continue to do our due diligence at utility commission proceedings to ensure they aren’t inflated for utilities’ financial gain, and also to ensure that some of these large loads aren’t “venue shopping” and being inadvertently double-counted in multiple utility planning proceedings.) But is the optimal way to meet that new demand locking in dirty fossil infrastructure for decades to come? Certainly not, particularly when the cost of cleaner alternatives has never been more competitive.

A smart portfolio of 1) much more aggressive energy efficiency and demand response/demand side management investments; 2) utility scale and distributed renewables and battery storage; and 3) optimized investments in both new and existing transmission (such as reconductoring) at the bulk and local distribution levels presents a much more financially and environmentally sustainable path. This cleaner, smarter approach is being actively explored and advanced in various utility proceedings by stakeholders, but without action and smart implementation, we’ll be left running headlong into more costly and dirty solutions.

The Southeast is at a crossroads. It is now incumbent on the region’s utilities, diverse stakeholders, state regulators, and lawmakers to come together and choose the right path forward—one that seizes the clear and present clean energy opportunity right under our noses, instead of racing headlong into a dead-end fossil fuel brick wall.

Related Blogs

The Global AI Buildout Needs Energy Transition Guardrails

The President Is Putting Oil First and America Last