The Pennsylvania Department of Environmental Protection will soon conclude the "pre-rulemaking" process for its proposed regulation to limit carbon pollution from power plants and enable the state to participate in the Regional Greenhouse Gas Initiative (RGGI). On May 7, the DEP brought regulatory language to its Air Quality Technical Advisory Committee (AQTAC) for an advisory vote; today it will present the language to its Citizens Advisory Council (CAC); and in July, the Environmental Quality Board will decide whether to initiate a formal rulemaking process.

Some AQTAC members supported the start of a carbon limits rulemaking; others opposed. A similar lack of consensus is expected at the CAC. Since many members of both bodies have ties to the coal and gas industries, such division is unsurprising. Nonetheless, the discussions there have been instructive in other ways. Not only have they highlighted that (with rare exceptions) coal and gas companies do not support meaningful climate change policies in Pennsylvania; they have also made clear how unprofitable the coal-fired electricity business has become in the commonwealth.

This blog discusses the reasons for coal's decline (mainly competition from cheap gas-fired power) and argues that while carbon limits may accelerate that decline by a couple of years, the best way for state policymakers to support impacted workers and communities is to support RGGI while also helping those workers and communities transition to a post-coal world, including through the use of RGGI auction proceeds.

Coal's Decline in the Commonwealth and the U.S., 2005-2020

When fracking arrived in Pennsylvania at the end of 2004, 55 percent of all the electricity produced in the state came from coal. By 2019 coal generation was down to 17 percent, while gas generation was up from 5 percent to 43 percent. This decline mirrors a nationwide trend. In 2011, according to the U.S. Energy Information Administration (EIA), the U.S. had 318,000 megawatts (MW) of coal plants and those plants operated at 67 percent of their capacity. By 2019, capacity had fallen to 229,000 MW and the remaining plants ran at a capacity factor of just 48 percent, with coal-fired generation reaching a 42-year low.

The reason for coal's fall is simple: it has become less expensive to generate electricity from gas and renewables. As a result, existing coal plants have lost market share in regional electricity markets, where power plants compete against each other to produce electricity at lowest cost, and utilities and developers no longer build coal plants. More and more they are deciding to build renewables, both because their costs continue to come down (especially when they are paired with energy storage), and because they produce electricity without carbon dioxide emissions. In January, the EIA forecast that 76 percent of the new capacity brought online in the United States in 2020 will be wind and solar plants.

In Pennsylvania and the PJM Interconnection region, though, the great majority of all of new power generation built during the fracking era has been gas-fired. And this wave of highly automated, low-labor-cost combined-cycle gas plants is drowning Pennsylvania's coal plants.

Pennsylvania Gas Is Killing Pennsylvania Coal

In 1996, Pennsylvania "restructured" its electric power sector, forcing electric utilities to spin off the power plants they owned to other companies to compete on PJM's electricity markets. Most of the plants spun off were coal plants (five were nuclear plants) because until very recently coal was generally the state's cheapest electricity source—much cheaper than gas. Moreover, most of cold plants were already relatively old, built in the 1960s and 70s.

Over the decade that followed restructuring, little new electricity generation was built in Pennsylvania. Then, as I discussed in a two-part blog last summer, and S&P Market Intelligence examined at length in a five-part series last December, fracking made gas cheap, and private equity funds, hedge funds, and other investors saw an opportunity. By building new, highly efficient combined-cycle gas power plants investors could out-compete the old coal plants on PJM's gas-friendly markets and make a lot of money—and they have. The result is that since 2010, 13,678 MW of new gas plants have come online in Pennsylvania and 9,097 MW of coal plants have retired. Thousands of additional MW of new gas are in PJM's generation queue.

Of course, gas is not the entire cause of coal's decline in Pennsylvania. Flat electricity demand and the Environmental Protection Agency's 2011 Mercury and Air Toxics Standard (MATS) rule have also contributed. But contrary to the suggestion of the U.S. Chamber of Commerce, those factors have played very minimal roles. Two recent studies, available here and here and discussed in a report by the External Environmental Economics Advisory Committee, found that cheap gas has accounted for 80-92 percent of coal plant retirements, with just 8-20 percent due to MATS and other factors. In other words, gas-fired generation would be driving coal offline even without MATS.

RGGI's Impact

Will Pennsylvania's coal plants survive until January, 2022, the earliest the state could start participating in RGGI? It's an open question because the COVID-19 recession has hit coal plants hard by significantly cutting electricity demand (since coal plants are relatively expensive, they run only when demand is relatively high). Last week, the EIA projected that U.S. coal generation in 2020 would be 25 percent less than originally forecast. As a result Pennsylvania may see some of its remaining coal plants retire before 2022 even without RGGI.

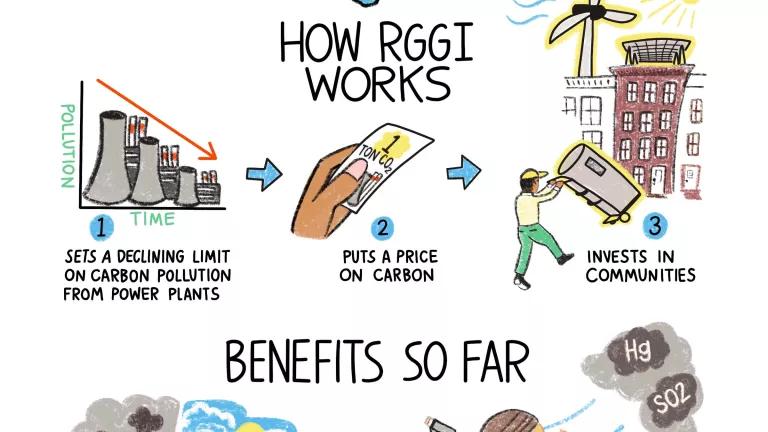

That said, to the extent the state's coal plants survive until 2022, Pennsylvania's participation in RGGI will certainly make them even less competitive. According to the DEP's modeling, the coal plants are so marginal that even a small price on carbon will push any remaining coal plants into retirement a couple years earlier than they would otherwise retire.

Understandably, this is a real concern for the Pennsylvanians who work in coal plants and the communities that depend on those plants, even though on a statewide basis the benefits of participating in RGGI would far outweigh the costs. Those benefits include supporting thousands of jobs at Pennsylvania's four nuclear facilities (in anticipation of RGGI, Energy Harbor has announced that it would keep the Beaver Valley nuclear plant open); improved public health due to decreased emissions of sulfur dioxide, nitrogen oxide emissions, and air toxics; a decrease of some 180 millions of tons of carbon dioxide emissions; and new jobs and economic development from the investment of RGGI proceeds through the Clean Air Fund.

Based on the public comments made at the May 7 AQTAC meeting, many coal plant workers recognize that new gas plants will soon eliminate their jobs, even without RGGI. But they still oppose RGGI (though, curiously, not gas) because in an economy that was creating few good-paying jobs for blue collar workers even before the COVID recession, "[m]any questions need to be answered on transition," in the words of one IBEW member.who spoke at AQTAC. In the meantime they want to keep their jobs as long as they can.

What the General Assembly Could Do Instead of Fighting RGGI

The implication of the IBEW worker's question was that the DEP should address transition in its proposed regulation. But the General Assembly has given the DEP few tools to do that under the Air Pollution Control Act. And the Competition Act eliminated the Public Utility Commission's jurisdiction over power sector planning, and therefore power plant closures. (By contrast, commissions in states like Michigan, where power plants are owned by PUC-regulated utilities, can and sometimes do require transition planning in connection with closures).

Under a "stakeholder capitalism" of the kind that the Business Roundtable nominally endorsed last summer, power companies might do transition planning voluntarily. Until that starts to happen in practice, we need policy to require such planning when power plants close, along with public investment to support the impacted workers and communities. Similarly, we need policy to ensure that both the emissions benefits and the investment benefits of RGGI are distributed where they are most needed: to communities affected by the transition from fossil fuels, communities of color, low-income Pennsylvanians, and other vulnerable communities that have historically borne a disproportionately high pollution burden.

The proceeds of RGGI allowance auctions would provide one source for that investment—but the investments must all contribute to the elimination of air pollution, unless the General Assembly authorizes a broader range of investments. A severance tax on natural gas, the main driver of coal plant closures, is another potential source. So far, however, state legislators with coal plants in their districts have shown no interest in supporting such investments, despite their (by all appearances) earnest desire to help their constituents. Instead they offer false solutions—such as opposition to RGGI—to coal plant closures, and so do a disservice to both current and future generations of Pennsylvanians.

Related Blogs

Energy Week: "Inaction Is Not an Option"

Pennsylvania Needs RGGI Now More Than Ever