US Needs to Reform International Finance System for Climate Action

Nearly two dozen groups are urging the Biden-Harris Administration to help revamp the international financial institutions for strengthened climate action.

In a letter, leading development, faith-based, environmental, science, foreign policy and other organizations identify three priority reforms the U.S. should champion to reform the international financial institutions (IFIs) for greater climate action. Administration has a once in a generation opportunity to deliver the needed reforms to simultaneously address global climate inequities, channel resources for climate-resilient development and mitigation efforts in developing countries, and unlock tens of billions of dollars per year for climate-smart development investments.

This letter is coupled with an advertising campaign in key media outlets to urge the U.S. administration to seize the near-term opportunity to lead on this agenda under the banner: It's Time to Change How the World Finances Climate Action.

The World is Calling for Action and the US is Poised to Lead

As the mounting climate crisis collides with the developing country debt crisis, pushing many millions of people further into poverty and other hardships, the need for reform is a matter of urgency. There is a growing push to deliver these reforms from the Bridgetown Initiative, and the Accra-Marrakech Agenda, to the decisions from the 2022 climate summit in Egypt. The United States is a major shareholder in all the IFIs that are critical to unlocking reforms and a significant player in global capital markets, so must rally the international community with greater urgency and ambition.

Transforming Multilateral Development Banks Can Unlock Financing

Key shareholders and stakeholders are urging multilateral development banks (MDBs) to significantly increase the quality and quantity of their climate finance, make modifications so that they are “fit for purpose” to address the climate crisis, and take more risk in helping to combat the myriad crises the world is facing. The MDBs are already a significant financier of climate mitigation and adaptation in developing countries, including the most vulnerable of them. Climate finance from MDBs to developing countries ($58.9 billion) rose by $13.5 billion between 2020 and 2021.

But the MDBs could do much more, by:

- Aggressively implementing the recommendations of the G20 Capital Adequacy Frameworks (CAF) review;

- Enabling MDB concessional investments in adaptation and loss and damage in a broader range of vulnerable countries; and

- Ensuring the quality of WBG financing is fully aligned with the Paris Agreement 1.5°C goal.

These three reforms could unleash more and better climate finance from the MDBs.

By pushing the World Bank Group (WBG) to change its equity-to-loan ratio target to at least 17-18%, the US could unlock an additional $4-8 billion per year with an additional $1.4-2.8 billion that could flow to climate activities (see table). This would unleash significantly more resources than the $4 billion per year that the WBG agreed when it recently changed its equity-to-loan ratio from 20% to 19%.

Additional lending capacity and climate finance associated with changes to the WBG equity-to-loan ratio

And by ensuring that its finance moves beyond only the “do no harm principle” to one that also maximizes the climate benefit from every dollar it invests, the WBG could unleash additional transformational climate action in developing countries. That means investing in renewable energy, not fossil fuels. For example, those increased and targeted investments could help unleash the 1.5 terawatts (TW) per year of new installed wind and solar capacity that the world needs through 2030 to meet our climate goals and deliver energy access for all.

At the same time, some of the most climate-vulnerable countries aren’t eligible for MDB concessional financing; they are dependent on more expensive financing to fund adaptation and address losses and damages from climate impacts. As today’s letter laments: “This is unfair and unjust – these countries have contributed little to the emissions fueling climate impacts that are causing rising adaptation needs and loss and damage costs.”

The MDBs also could reform some of their criteria so that all climate-vulnerable countries can access temporary WBG concessional financing for “external shocks” such as extreme weather events. And supporting an “adaptation carve out” at the MDBs would allow all vulnerable countries to access more concessional finance for adaptation investments.

Special Drawing Rights Are Another Key Tool

In August 2021, the International Monetary Fund (IMF) approved a general allocation of 456.5 billion in Special Drawing Rights (SDRs) – approximately $650 billion USD – to its 190 government members, apportioned according to each country’s shareholding. This was only the fourth time the IMF has made a general allocation of SDRs. As an international reserve asset, SDRs can provide much-needed financial liquidity for countries facing economic challenges due to the compounding climate, debt, energy, food, and public health crises and other acute challenges. While many rich countries do not need their SDRs and they would go unused without action, allocations of SDRs help developing countries provide low-cost finance to meet urgent needs, including those caused by climate-fueled fueled disasters. In the latest round of SDRs issuance, over 99 developing countries used their SDR allocation. In addition, several developed countries committed to re-channel their unused SDR allocation to two IMF trust funds – the Poverty Reduction and Growth Trust and the Resilience and Sustainability Trust – that will use these SDRs to provide low-cost financing to poorer countries that need it.

While the U.S. continues to support efforts to re-channel a portion of the U.S. allocation of SDRs issued in 2021, they should also:

- Encourage rich countries to re-channel SDRs and support innovative proposals for how IFIs can deploy them, such as SDR-denominated bonds or hybrid capital facilities; and

- Support another round of SDR issuance.

Mobilizing these actions around SDRs could help provide developing countries with relatively low-cost financing that they could use for greater climate action.

Using innovative tools such as SDR-denominated bonds would help countries – like the United States and several European countries – better utilize their SDR allocations as they argue they currently face legal hurdles to re-channeling their SDRs to MDBs. Such an approach would help the World Bank expand its lending capacity by a significant amount, without needing additional resources from the U.S. Congress.

The United States could also help developing countries tap into much lower cost finance than they can secure on the global market by supporting a new issuance of SDRs. Another issuance of SDRs would create liquidity support of $212 billion for emerging market and developing countries, with $21 billion of this going to the lowest income countries.

Championing Debt Reforms for Climate Action

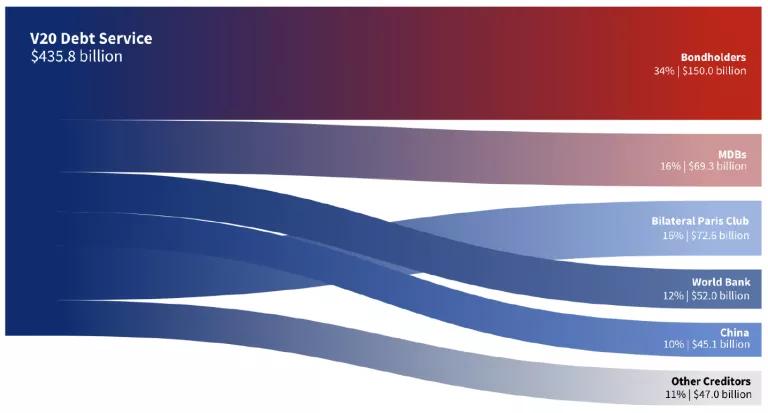

A growing number of developing countries are struggling with unsustainable sovereign debt which is a result of long-standing inequities in the global financial and economic system, now exacerbated by climate disasters. This challenge is very real as the V20 – a group of 58 of the most climate vulnerable countries in the world – will be required to make almost $435.8 billion in debt payments to various creditors between 2022-2028 (see figure).

Figure: V20 Debt Payments by Creditor

Source: V20 Debt Review

Climate change will make this debt challenge even more inequitable. Developing countries often need to take out new loans to address the impacts of climate disasters, further increasing their debt distress. As a recent report for the V20 stated:

“When scarce public finances are mostly spent on paying debt service rather than making the necessary investments to build a more resilient economy, the most vulnerable countries will be locking themselves in a cycle of unsustainable debt further fueled by climate impacts.”

The U.S. can begin to help address these debt challenges by:

- Delivering on debt restructuring by supporting mechanisms where all debt holders – including the private sector – take a “haircut” on their loans as a part of a debt restructuring agreement, so repayment is more sustainable;

- Spearheading scalable solutions for debt for climate/nature swaps; and

- Spurring the inclusion of natural disaster clauses in all debt instruments.

Driving forward these three actions around debt could help the most vulnerable countries use scarce resources to help make smart climate investments instead of making unstainable debt payments to creditors.

While there are efforts to provide debt relief – such as ongoing negotiations for Zambia, Ghana, and Sri Lanka – they are widely viewed as ineffective. As the letter states: “The current G20 Common Framework process to restructure sovereign debt is not delivering, and needs to provide more efficient, predictable and clear processes to accelerate restructuring.” There are some stepped up efforts to encourage major creditor countries like China and private lenders to renegotiate debt terms, so they are more sustainable. For example, New York State is considering a bill that would pressure private creditors to come to the negotiating table and agree to equitable debt restructuring.

And while not a panacea, including “natural disaster” clauses in all debt instruments is an important step to alleviate some debt burdens. These provisions would “suspend the debt service for two years when an independent agency declares a natural disaster of a certain threshold has hit and extends the instrument’s maturity for two years at the initial interest rate”. This allows developing countries hit by climate impacts, which they did little to cause, the fiscal space to prioritize vital investments in disaster response and recovery. The U.S. has recently indicated that it supports including these in all debt instruments – including those issued by the MDBs and private creditors – so the U.S. should play a key role in ensuring such provisions are widely used in future sovereign debt contracts.

Efforts are also underway to provide “debt-for-nature/climate swaps” where countries reduce their debt burdens in exchange for using the savings for investments in nature protection or increased climate actions. The U.S. has supported these efforts with a recent debt-for-nature swap in Ecuador – the world’s largest to date – that uses the resources from the reduced debt payments to create and maintain a marine protected area in the Galápagos Islands.

Without further measures to address the debt crisis, it is very difficult to envision how vulnerable countries can make investments in climate action given their current debt burden and the likely increased debt that will materialize if the world doesn’t act more aggressively on climate change.

The United States Must Champion these Essential Reforms

As world leaders focus their attention on reforming the international financial system, the U.S. urgently needs to step-up its leadership to drive these targeted reforms. As it shows up at global forums – such as the Summit for a New Global Financial Pact in June, the G20 Summit in September, the World Bank/IMF Annual Meetings in October, and COP28 in December – the U.S. needs to transform the MDBs, catalyze the larger use of SDRs, and spur greater debt reforms for climate action.

The Biden-Harris Administration can use its leadership to deliver these reforms with the tools the U.S. already has.

Related Blogs

COP29: Key Outcomes Signal Need to Deliver Greater Climate Action

Driving Ambition, Action, and Equity at COP28 (Part 2)