Choosing a Home with Climate Change in Mind

Worried about how your new place will hold up in the face of extreme weather? Here’s what to look out for before you settle down.

Flooding in Lindenhurst, New York, January 13, 2024

J. Conrad Williams Jr./Newsday RM via Getty Images

As the impacts of climate change become increasingly evident, more people are thinking about how well their home—and wallet—will fare through intensifying flooding events, hotter weather, prolonged droughts, and changing winters. And for those prospective buyers or renters in the house-hunting process, the question of climate resiliency is now a common safety consideration.

While some places in the United States are more prone to specific climate threats (e.g., hurricanes in the Southeast, wildfires in the West), no place is immune to the impacts of climate change. And most of us are already paying the costs, whether that’s through heftier utility bills (as happens with increased AC use) or soaring insurance premiums.

Despite the unknowns, though, there are plenty of precautions you can take before you decide on your home, with climate concerns in mind.

Get an overview of potential climate risks

Start by looking online for public data about the house or building you’re considering, as well as the neighborhood. Among various other sites that offer useful information, First Street Technology gives users a quick, free snapshot of climate risks for a piece of property, based on the address you type into a search bar and computer model predictions. (Note that this data is not based on actual occurrences of flooding or wildfires, etc., but provides scores for projected flood, fire, wind, air, and heat risks.) Once you have a better understanding of what you might be facing, you can start to dig further into the history of the property. Some real estate sites, like Realtor.com and Redfin, incorporate First Street’s climate risk details directly into home listings.

Learn about the property’s flood history

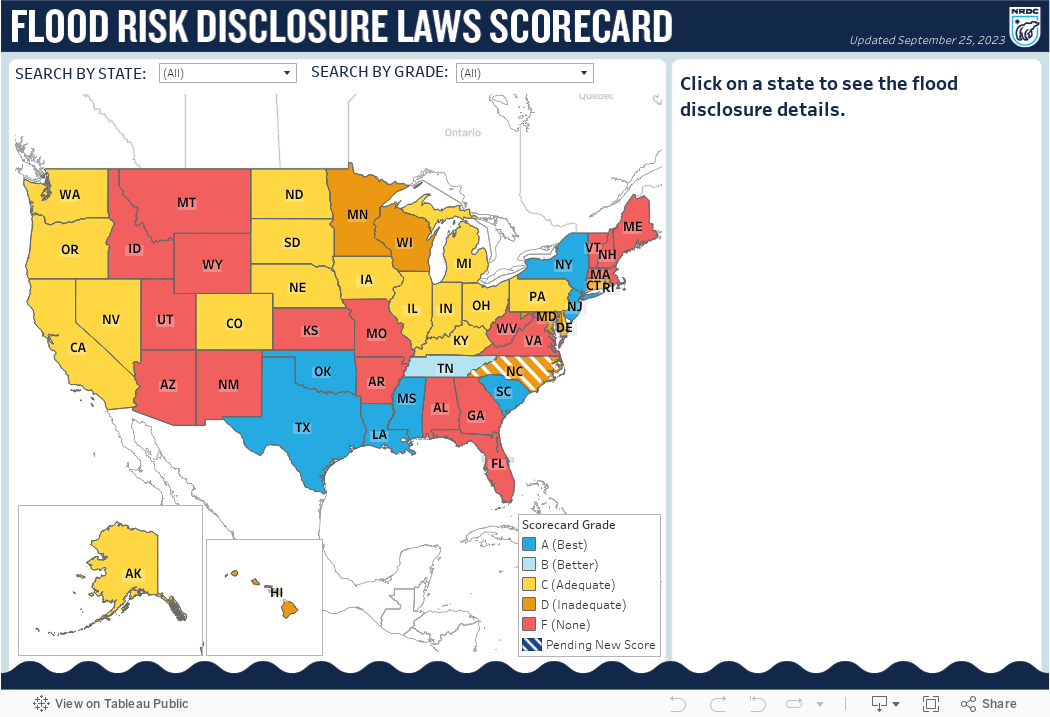

Flooding can cause costly damages, and as the frequency of extreme storms increases, so will the cost of your insurance premiums. It’s critical to find out whether a potential home is prone to flooding, but unfortunately, more than a third of U.S. states do not require sellers to disclose a property’s flood history or flood risks to buyers. NRDC’s flood risk disclosure laws scorecard map provides an overview of which states have these policies in place and which types of information (if any) must be disclosed during the purchase or rental process.

If you live in a state with no disclosure requirements, however—e.g., Arizona, Georgia, New Mexico, and Virginia—you will have to probe for more information on your own. Below are some sample questions you can try asking the seller (or landlord).

- Has there ever been any flooding on the property? If yes, how many times, and did the incidents cause major damage, such as foundation cracks or buckling floors?

- Do you have flood insurance, or is there a mandate to have flood insurance for the property?

- Is the property in a flood hazard area, designated flood zone, or wetland area?

- Have you ever received federal disaster flood assistance for flood damage on the property?

Learn More: Floods & Wildfires

Note that your prospective new neighbors may also be open to sharing information about past storm incidents. This can be especially helpful if you’re considering a home that was recently flipped, since the flipper only has to disclose what they know in their short period as property owners. Long-time residents of the area could help you fill in the gaps.

Make use of property and neighborhood reports from FEMA and other agencies

The flood maps maintained by the Federal Emergency Management Agency (FEMA) are outdated and unable to provide an assessment at a property level, but they do offer more zoomed-out information. If your potential home is in a zone coded with the letters A or V, it means it is considered a Special Flood Hazard Area, with a high risk of flooding. And if it’s part of a community that participates in the National Flood Insurance Program, you, too, will be required to buy flood insurance. If your home is located in a zone coded with letters B, C, or X, it means it is in a Non-Special Flood Hazard Area with moderate or low-risk flooding.

To dig deeper, you can also request a Comprehensive Loss Underwriting Exchange (CLUE) report online, which details select insurance claims on a property for the past seven years. Keep in mind, though, that not every insurance company participates in submitting information to the CLUE database, and some owners don’t document damages to their property. But the report could bring to light some potential issues with the property, including flood damage.

FEMA now offers a useful tool that allows anyone to get a quote on flood insurance premiums, which can clue you into flood risks (i.e. expensive insurance means it’s a high-risk property).

Look up the elevation of the property to gauge its flooding resiliency and inspect the grounds

FEMA uses base flood elevation—a gauge of how high the surrounding water levels might rise during a storm—to decide how at risk an area is for flooding. Various smartphone apps can clarify where your home is situated relative to sea level. On an iPhone, use the Compass app or Apple Maps; on an Android, try Google Maps. Keep in mind, though, that areas at high elevations can still see devastating floods too; take the damage suffered by the residents of the mountainous areas of western North Carolina due to Hurricane Helene as an example.

You can also do some investigating IRL. If possible, wait for a rainy day to see whether there are any low spots on or around the property that collect water. And take some time to explore the neighborhood. Are there any underpasses or streets that flood easily and would impact your route to work or school or your access to emergency services? If the home happens to be situated at the bottom of a hill, are the sewage drains working properly?

Clockwise from top left: A family looking through their belongings after their home was flooded by heavy rains from Hurricane Harvey in Houston, Texas; a for-sale sign of a home in the Fountain Grove area of Santa Rosa, California, after a wildfire in Sonoma County; the Blue Ridge Fire—shown here engulfing the town of Chino Hill, California in October 2020—and Silverado Fire spread across thousands of acres.

Erich Schlegel/Getty Images

; 2)Paul Kitagaki Jr/Sacramento Bee/ZUMA Wire/Alamy Live News

; 3)David McNew/Getty Images

Suss out your area’s wildfire risks

Information on wildfire dangers for potential homeowners is pretty limited. Only two states, California and Oregon, have wildfire risk disclosure policies in place. But two federal tools provide some helpful insights.

- The USDA Forest Service’s Wildfire Risk to Communities: Though it is not specific enough to be used for gleaning risk factors to individual properties, this website features maps, charts, and resources applicable to a given community, county, Tribal area, and state.

- The National Interagency Fire Center: This site has maps for current wildfires, wildfire forecasts, and droughts as well as data for historical wildfires across the country.

Investigate hyperlocal wildfire safety measures and risk factors

When doing some DIY surveyor work around the property, ask yourself these questions:

- Have previous owners done any fireproofing in and around the home already? Take a look at the condition of the windows and roof. (You might need to consult with a professional about the materials and what would work best in a fire-prone area.)

- Is the property close to or located in the wildland-urban interface, i.e., near any undeveloped land that can more easily catch on fire?

- Where is the closest water source and is it accessible to the fire department in the event of an emergency?

- Are there multiple routes for accessing and evacuating the property, in case one route is blocked via fires or fallen debris?

- Ask the local fire department about the fire history of the neighborhood and whether there’s a community emergency wildfire plan in place. Some communities have banded together to implement collective fire safety measures, with help from resources like Firewise USA.

Assessing damage potentially caused by flooding in a basement

Alex Potemkin/Getty Images

Consult with professionals

Of course, there is only so much you can do to find out about the property on your own. In some cases, it would be worth shelling out for a property inspector to give you the nitty-gritty of the interior and exterior, including hidden issues like water damage, mold, and other structural issues caused by past flooding or fires. This type of expert could also evaluate the resiliency of your home’s foundation.

Insurance agents are another resource to tap for professional advice on a property. Reach out to an agent to get an estimate on the recommended insurance. This will not only give you a better picture of the monthly living costs but also provide some insight into potential persistent risks that the property might face.

Finally, the local or county emergency management office can tell you if a neighborhood has a history of storm damage. (They may be limited in what they can say about an individual property, however.)

Note any opportunities for mitigating climate risks and/or decarbonizing your lifestyle

Moving into a new home means new opportunities to take on greener habits. Start with this checklist:

- Is there green landscaping around the home—which could include trees, shrubs, and ground-cover plants—shading the exterior? In a hot climate, these features are helpful in reducing heat radiation and providing natural cooling. (They can also be lifesaving in the event of a heat wave–related power outage.) Likewise, green infrastructure can help reduce your home’s risk of flooding. This can include rain gardens or downspout disconnection, the practice of redirecting rooftop runoff from storm drains to lawns, rain barrels, or cisterns, which capture and hold the water.

- Is the home wired for electrical appliances, such as an electric or induction stovetop?

- Is the home set up for renewable energy? For example, is it outfitted with solar panels?

- Is the home fitted with a smart thermostat? These appliances can help you save an average of 8 percent on your utility bill.

- How is the home heated and cooled? Keep in mind that the most cost-efficient time to switch over to an energy-efficient heat pump is when you need a new AC; avoid waiting until your gas furnace or boiler goes out to upgrade a heating system.

With the right features, your home and its surrounding property can also have a better chance of withstanding climate impacts.

This NRDC.org story is available for online republication by news media outlets or nonprofits under these conditions: The writer(s) must be credited with a byline; you must note prominently that the story was originally published by NRDC.org and link to the original; the story cannot be edited (beyond simple things such as grammar); you can’t resell the story in any form or grant republishing rights to other outlets; you can’t republish our material wholesale or automatically—you need to select stories individually; you can’t republish the photos or graphics on our site without specific permission; you should drop us a note to let us know when you’ve used one of our stories.

How to Stay Safe From Wildfire Smoke

What It’ll Take to Save Cities like New Orleans from Climate Disaster

What Are the Solutions to Climate Change?